Weekly Newsletter April 6th to April 10th

RECAPPING LAST WEEK

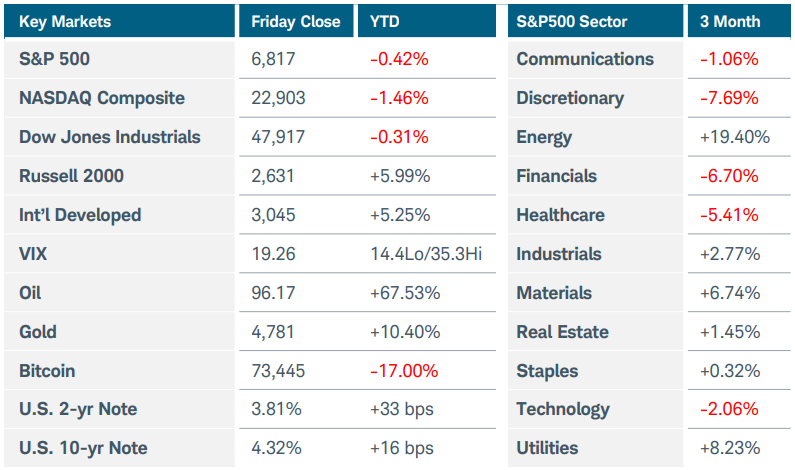

U.S. equity indices rallied sharply for a second straight week after the U.S. and Iran agreed to a two-week ceasefire, with the Nasdaq Composite index soaring 4.7%, while the Russell 2000 jumped 4% and the S&P500 rose 3.6%. The truce is tenuous though, as Israel’s ongoing attacks in Lebanon were seen as a violation of the ceasefire terms, and the Strait of Hormuz remained effectively closed. Crude oil futures tumbled from earlier highs above $117 to end the week more than 14% lower at $96.17. Brent futures also plunged, sending emerging market equity indices rocketing higher by nearly 8%. Energy was once again the sole loser among U.S. sectors, while technology, industrials, and consumer discretionary all recorded strong returns. Within the technology sector, semiconductors soared more than 13% to an all-time high, but software sank 7% after Anthropic held back the release of a powerful AI model over concerns it could expose vulnerabilities in traditional software programs. In economic news, March’s CPI report revealed the first inflation effects from the Iran war. The consumer price index rose 0.9% MoM and 3.3% YoY, in line with estimates but the highest annual rate in two years. The jump in gasoline prices accounted for nearly three-quarters of the increase. Core inflation rose just 2.6% YoY, confirming that the war’s inflation impact has not yet spread beyond energy prices. U.S. Treasury yields were flat at the short- and intermediate-term durations as traders clung to slim hopes for at least one rate cut this year, while long-term yields rose after a 30-year auction drew slightly weaker-thanexpected demand. Minutes from last month’s FOMC meeting revealed a growing consensus among policymakers that taming inflation could require rate hikes. U.S. consumer sentiment sank to 47.6, a record low reading, as one-year inflation expectations jumped to 4.8% from 3.8%. Growth in the services sector slowed in March while prices paid by businesses climbed to a 3-1/2 year high and supplier delivery times increased. The final reading of Q4 2025 GDP slipped to 0.5% growth, down from the first two estimates of 1.4% and 0.7%. The Atlanta Fed’s GDPNow “nowcast”—which is not a forecast but rather an up-to-date reflection of data releases—sits at 1.3% growth for the first quarter of 2026. The government’s first official GDP estimate will be released on April 30. Overseas, OPEC+ agreed to a modest production rise for May, though if Middle East supply disruptions continue that move would have little impact. China’s producer prices rose for the first time in more than three years as the war in Iran started to drive up cost pressures. Consumer prices eased slightly, rising 1% YoY in March versus 1.3% prior. In the Eurozone, investor confidence fell to a one-year low of -19.2 as recession fears escalated. March’s final PMI reading reflected higher energy costs and disrupted supply chains.

THE WEEK AHEAD

Late last week, Iran said that its frozen assets in foreign banks must be released and that a ceasefire in Lebanon be established before peace talks could proceed, casting doubt on U.S.- Iranian negotiations scheduled for over the weekend in Pakistan. Israel had expressed willingness to negotiate with Lebanon, but the two countries continued to exchange strikes on Friday, keeping global markets on edge. This week is light on economic data, so developments in the Middle East and oil prices are likely to set the tone again. U.S. investors’ attention will turn to the beginning of first quarter earnings season to see how business outlooks might be affected by the war. Most of the major U.S. banks will report along with technology companies ASML Holdings, Taiwan Semis, and Netflix. The domestic economic calendar includes producer prices, existing home sales, industrial production figures, and regional manufacturing surveys. There will be many appearances by FOMC members throughout the week. On the international side, China reports Q1 GDP and monthly industrial production, and retail sales numbers on Wednesday evening. None of those data points are likely to reflect the full impact of the Iran war. The International Monetary Fund’s bi-annual meeting convenes in Washington amid high uncertainty and volatility for global economies. Australia’s employment report and the UK’s GDP update round out the calendar.

CHART OF THE WEEK

Overseas momentum

The flagging U.S. dollar and subsequent outperformance of international equity markets versus the U.S. has been a major investing theme over the past year. That thesis took a hit when the Iran war started but resumed in earnest after last week’s ceasefire announcement. The chart below contrasts the returns of the MSCI EAFE index (MXEA), representing developed economies, and the MSCI Emerging Markets index (MXEF), over the past year. Recently, both bottomed out a week before the ceasefire, but that news is what triggered a textbook risk-on cascade of reactions. Oil prices fell sharply, reducing global inflation expectations, and triggered a broad rotation back towards equities. Emerging markets, especially in Asia, are particularly sensitive to the energy supply issues that the war created. These economies roared back last week after taking the brunt of the pain at the beginning of the conflict. MXEF and MXEA rallied 7.7% and 4.4%, respectively. Both moves are significant but the performance gap between them is widening once again as emerging markets continue to surge. The currencies and local rates of those countries moved favorably as capital flowed back to higher-yielding and commodity-levered economies. International emerging markets consistently outperforming developed economies reflects investors’ improving risk appetite despite the geopolitical turmoil. A similar phenomenon is playing out in the U.S., with small-cap stocks outperforming large-cap by a sizable margin over the past year. Of course, all these developments are heavily dependent on whether the situation in the Middle East comes to a lasting resolution.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.