Weekly Newsletter August 11th to August 15th

RECAPPING LAST WEEK

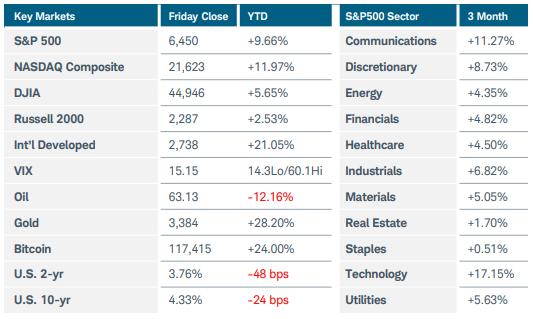

Investors’ growing confidence on interest rate cuts propelled the S&P500 and Nasdaq Composite indices nearly 1% higher to new record weekly closes despite mixed inflation data. The Russell 2000 jumped 3%, and international stocks posted solid gains. An extension of the tariff truce between the U.S. and China also boosted sentiment. Seven of eleven S&P500 sectors finished positive, led by healthcare, communications, and discretionary. Crude oil prices were little changed even as OPEC raised its global oil demand forecast for 2026 and lowered its estimate for U.S. supply growth, suggesting a tighter market. Gold futures fell 2% as traders awaited further clarification on whether gold bars would be subject to U.S. tariffs. Ethereum continued to dominate cryptocurrency flows, surging 18% before settling for an 8% weekly gain. U.S. Treasury yields initially moved lower after Tuesday’s CPI report, which revealed that consumer prices increased only moderately last month. That news also sent equity indices sharply higher as rate cut expectations increased. However, Thursday’s producer price index report showed a 0.9% jump MoM due to a large increase in services and food prices, a result in line with economists’ view that tariffs continue to pose higher inflation risks. Two-year Treasury yields—a good proxy for where investors think the Fed funds rate is headed—fell to a three-month low of 3.66% before ending the week modestly higher at 3.76%. Meanwhile, the odds of a September rate cut—which approached 100% after the CPI report—still stood near 85% at week’s end, despite the upsurge in wholesale prices. In other economic news, U.S. consumer sentiment sank to 58.6 this month, well below estimates of 62.0. Inflation expectations were the main reason for the drop, as the one-year outlook rose to 4.9% from 4.5%, while the long-run view increased to 3.9% from 3.4%. Retail sales, which are not adjusted for inflation, grew 0.5% last month, and the June figure was revised up to 0.9%. Overseas, China’s industrial production and retail sales figures for July missed forecasts, raising pressure on the government to create additional stimulus measures to stoke domestic demand. Japan’s economy expanded at a better-then-expected 1% annualized pace in Q2 and 0.3% QoQ as export volumes performed well in the face of tariffs. Australia’s central bank lowered rates by 25 basis points to 3.60% on Tuesday while downgrading the country’s economic outlook. Another rate cut is expected later this year even as wage growth remained elevated. Finally, Eurozone GDP grew by just 0.1% in Q2 as industrial output dipped, while Britian reported growth of 0.3% after a 0.7% expansion in the prior quarter.

THE WEEK AHEAD

On the geopolitical front, President Trump met with Russian President Putin over the weekend to discuss a ceasefire deal, with Ukrainian President Zelensky headed to Washington today. Looking at this week’s economic agenda, all eyes will turn to the Kansas City Fed’s annual three-day symposium, which begins Thursday in Jackson Hole. This gathering is always viewed as an important signpost for future Fed policy, and this year will be no different, given recent developments in the U.S. jobs and inflation data, and the political pressure coming from the current administration. Fed Chair Powell is scheduled to speak on Friday morning. Additionally, minutes from this month’s FOMC meeting will be released on Wednesday. August’s flash PMI data arrives this week and will be the first insights into how the latest round of tariffs are affecting the world’s major developed economies. There is a slew of housing data on tap, including building permits and existing home sales. Last week, Warren Buffett’s Berkshire Hathaway revealed major purchases in U.S. homebuilding stocks, as well as in beleaguered healthcare conglomerate UnitedHealth Group. Earnings reports from retail giants Walmart, Target, and Home Deport round out the domestic calendar. On the international side, inflation updates from Canada, the UK, and Japan are some of the major releases scheduled, along with the flash PMI reports.

CHART OF THE WEEK

Small cap strength

The Russell 2000 index (RUT) has doubled the gains of its large-cap counterpart, the S&P500 index (SPX), thus far in August. Last week’s small-cap surge was reflected in the relative strength indicator. After underperforming SPX from last December through the April lows, RUT entered a phase marked by strong absolute performance, yet still only kept pace with the main U.S. equity benchmark. The small-cap index breaking out to an eight-month high last week was not confirmed by a similar move in relative strength versus SPX but bears monitoring. Interest rates have regained control of the narrative with investors expecting a September rate cut—this development is particularly important to the smaller companies in the RUT that generally carry higher debt loads at shorter durations. The prospect of lower borrowing costs boosts these companies’ growth prospects and tends to impact valuations quickly. This also can increase the risk appetite from investors looking to rotate out of large gains from the mega-caps into cyclicals, financials and industrials, all heavily represented in the Russell 2000 index. Lower rates can also decrease investor demand for bonds, offering another potential source of funds as rotation progresses. Ultimately, more clarity on the future path of rates along with improving earnings could lead to a more sustained period of outperformance.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.