Weekly Newsletter August 18th to August 22nd

RECAPPING LAST WEEK

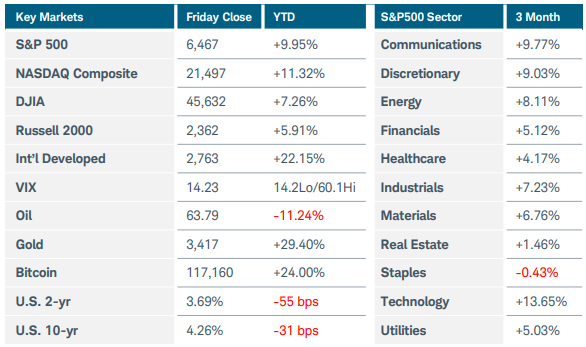

U.S. equity indices finished the week on a strong note, while Treasury yields and the U.S. dollar index tumbled after Federal Reserve Chair Powell signaled that the central bank is likely ready to resume interest rate cuts next month. The S&P500 index overcame earlier weakness caused by retailers’ mixed earnings reports to finish marginally higher while the Nasdaq Composite fell 0.5%, dragged down by concerns around artificial intelligence-related valuations. The Russell 2000 soared nearly 4% on Friday as smaller companies with higher debt loads may benefit from looser Fed policy. Economically sensitive cyclical sectors also posted solid returns for the week. Commodities like gold and oil rose on the prospects of lower rates and a weaker dollar, while Ethereum rocketed 9% to a new record high. In his speech at Jackson Hole, Powell said that “with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.” Odds for a September rate cut—which had fallen below 70% before the speech—jumped to over 90% before settling near 83%. Two-year Treasury yields slid to 3.69% while the 10-year closed near 4.26%. Powell stated that downside risks to employment have risen but also cautioned that the central bank must still guard against the inflationary effects from tariffs. While not exactly dovish, the speech was less hawkish than investors had feared. He also outlined changes to the Fed’s monetary policy framework, removing language about the pre-2021 low-rate environment and returning to flexible inflation targeting. In other economic news, U.S. manufacturing expanded this month at its fastest rate in over three years, with stronger demand also triggering pricing pressures. The S&P Global flash manufacturing PMI jumped to 53.3 while services eased slightly to 55.4. U.S. housing starts and permits rose in July despite high mortgage rates and an uncertain economy, while the growing supply of existing homes took some pressure off home prices. Retailer Home Depot missed expectations for quarterly revenue and profit but did not lower its future guidance. Walmart raised its sales and earnings forecast, noting that thus far, the tariff impact has been gradual enough not to have changed customer habits. Overseas, businesses in Germany and the wider Eurozone saw new orders increase for the first time in over a year, pushing the flash manufacturing PMI to its highest level in more than three years. British composite PMI surged to 53.0, but inflationary pressures returned as CPI jumped to 3.8% YoY in July from 3.6%. Services inflation spiked to 5%YoY, likely pushing back any chance of further rate cuts to spring 2026 at the earliest. Finally, Japan’s core CPI slowed to 3.1% YoY last month as food prices continued to ease.

THE WEEK AHEAD

With investors seemingly more confident in the Fed’s policy path, their attention will likely turn to the jobs and inflation data due before the next FOMC meeting. First up will be this week’s PCE price index, set for release on Friday. Last week Powell said that he believes that inflation effects are likely short-term, a view not necessarily shared by other members of the committee. The PCE release will be scoured for indications either that businesses are continuing to absorb price increases, or that they have begun passing them through to consumers. The headline inflation number has declined recently, even as core readings and producer prices rise. This week the second estimate of Q2 GDP arrives, along with this month’s final consumer sentiment and inflation expectations. Other releases on the U.S. calendar include consumer confidence, new and pending home sales, and goods trade balance figures. Last week’s wobble in technology stocks puts an even bigger spotlight on Nvidia’s earnings report after the close on Wednesday. On the international side, inflation updates from the Eurozone, Japan, and Australia are the main economic releases to watch. Accelerating CPI could push the probability of a Bank of Japan rate hike this year even higher and boost the flagging yen. Minutes from the recent central bank meetings of Australia and Europe round out the calendar.

CHART OF THE WEEK

Optimistic waves

Since the April lows, the S&P500 index (SPX) has ground steadily higher. At the same time, momentum has been slowing, as evidenced by the MACD indicator making a series of lower highs. Some of the recent loss of momentum could be attributed to the uncertainty around the future path of interest rates. Friday’s speech from Fed Chair Powell reassured investors, re-igniting the bull market that was lying in wait. This expansion fits with the Elliott Wave analysis we discussed in last week’s webinar of a developing bullish wave 3 within a larger wave 5. According to Elliott Wave Theory, bull markets develop in 5 waves—three impulse waves along with two corrective waves. Although SPX is potentially in that final wave on a larger degree, it has not yet reached its destination. Projections can be difficult to estimate with the index in uncharted territory, but Fibonacci extensions may provide a framework. In this case the extensions are pointing to the area near $6,800 (indicated by the grey box in the chart) for completion of this wave 3, which could be followed by a corrective wave 4 and then a bullish wave 5. That pattern could ultimately carry SPX above $7,000. However, momentum has not fully resurfaced yet. The MACD will likely have to break above its mid-August high to confirm the index’s continued push to record highs.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.