Weekly Newsletter December 15th to December 19th

RECAPPING LAST WEEK

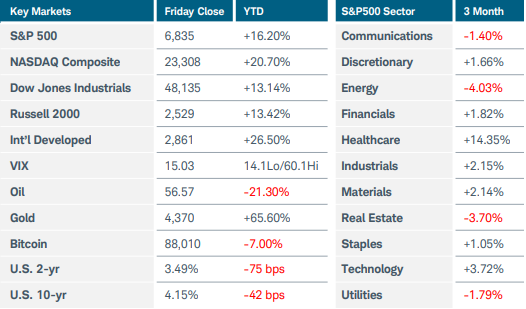

U.S. equity markets clawed back most of their early-week losses as investors sorted through long-delayed employment and inflation reports. The S&P500 and Nasdaq Composite indices ended the week slightly higher, while the Russell 2000 index slid less than 1%. Seven of eleven S&P500 sectors posted gains, but pressure on crude oil caused energy to tumble 3%. The possibility of a peace agreement in Ukraine that could bring Russian oil back to the market sent crude futures to near $55 per barrel, their lowest level since early 2021. Prices bounced back modestly after the U.S. imposed a blockade on Venezuelan tankers. Oracle’s news of potential financing issues with a new data center impacted technology stocks negatively, but they recovered by week’s end. Precious metals continued to shine as silver prices jumped another 8% while gold reached a new record high near $4,410. Economic data gave investors some hope that the Federal Reserve will continue lowering interest rates in 2026, sending U.S. Treasury yields lower. November’s non-farm payrolls report showed an increase of 64,000 jobs with the unemployment rate ticking up to 4.6%. The U.S. economy shed 105,000 jobs in October, reflecting the departure of federal employees that took deferred buyouts. Overall, the numbers were consistent with a gradually weakening labor market. Meanwhile, U.S. retail sales were flat in October as the government began the slow process of catching up on that important consumer spending data. Thursday’s November CPI report was the catalyst for the recovery in U.S. equity indices and further drop in Treasury yields. Consumer prices rose 2.7% YoY, well below expectations of 3.1%. However, because the October CPI report was cancelled, many of the usual data points were missing, and New York Fed President Williams cautioned that the headline reading was likely lower than it otherwise would have been. While odds for a FOMC rate cut in January remained low, prospects for a reduction at the following meeting in March improved moderately. In other economic news, this month’s U.S. business activity remained in expansion territory, though the pace of growth was the slowest since June. Respondents to the S&P Global flash PMI survey reported constrained job growth and a surge in costs for service firms. December’s final consumer sentiment index rose less than expected to 52.9, nearly 30% lower than a year ago. Lingering affordability issues weighed heavily as one-year inflation expectations sat at 4.2%. Overseas, the Bank of Japan raised rates to 0.75% from 0.50%, the highest level in 30 years. Government bond yields spiked to a 26-year peak, but the yen sank after BOJ Governor Ueda remained vague on the timing and pace of further hikes. The Bank of England cut rates by 25 basis points to 3.75% in a close vote and signaled only two additional cuts next year. UK inflation cooled more than forecasted to 3.2% YoY in November, supporting the central bank’s decision. The European Central Bank left rates unchanged and issued a more positive view of the Eurozone economy. Finally, China’s industrial production rose 4.8% YoY, the slowest pace since August 2024, as the country faces potential backlash from trading partners for its record trade surplus. Retail sales grew by just 1.3% YoY, the weakest since December 2022.

THE WEEK AHEAD

This will be the last issue of Macro Monday for this year, with the next publication on January 5, 2026. Investors are still hopeful for a year-end rally despite recent volatility caused by weakness in technology stocks and uncertainty around the Fed’s approach to monetary policy in 2026. Ongoing tensions between the U.S. and Venezuela also have the potential to destabilize global markets should the situation escalate. For this holiday week, most of the economic data will be released on Tuesday, ahead of Wednesday’s shortened market session and Thursday’s closure for Christmas. In the U.S., the focus will be on the long-delayed preliminary estimate of third-quarter GDP. Consensus estimates call for 3.2% growth, down from Q2’s 3.8% but still indicative of a healthy economy. Other U.S. economic releases will include consumer confidence, durable goods orders, and industrial production. No announcements are scheduled for Friday. On the international calendar, most of the news will flow from the Far East, with Japan reporting inflation figures and the release of last week’s BOJ meeting minutes. Looking ahead to the final week of the year, there are a few items on the docket worth noting, including the minutes from the recent FOMC meeting and China’s manufacturing and services PMIs, both on Tuesday, December 30.

CHART OF THE WEEK

A crude reality

U.S. consumer sentiment surveys have reflected a consistent theme in 2025: rising expenses. Falling oil prices, which have led to cheaper gasoline, have been the one exception and a bright spot for consumers. Since peaking at over $130 when war broke out in Ukraine in early 2022, oil has been in a steady downtrend. Looking at the S&P GSCI Crude Oil index ($SPGSCL), which tracks crude oil futures, technical support near $355 (around $65 per barrel on crude itself) held for several years. Each subsequent rally stalled out at consistently lower highs, creating a long and wide descending triangle technical pattern, which often precedes a break of support. That support held until the tariff scare in April. After the tariffs were paused in early June, oil attempted a bullish reversal but failed at the down sloping trendline, eventually falling to nearly five-year lows. Fears of oversupply have put continuous pressure on oil prices, outweighing geopolitical concerns. Reserves sitting on oil tankers are up 30% since August, and suppliers are reducing ship speeds since their destinations already have ample product. Barring shifts in macroeconomic factors, 2026 may continue to bring consumers some relief in the cost of petroleum-based goods.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.