Weekly Newsletter December 1st to December 5th

RECAPPING LAST WEEK

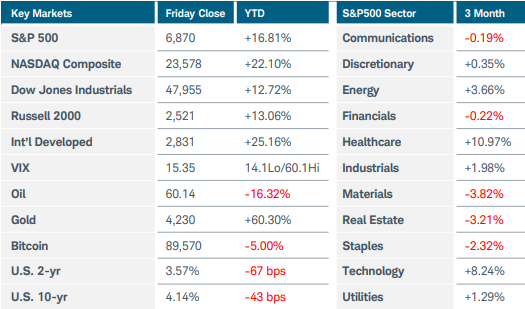

U.S. equity indices posted modest gains as investors’ expectations for an interest rate cut this month continued to rise. The Nasdaq Composite and Russell 2000 indices each rose nearly 1%, while the S&P500 added 0.3%. Sector performance was mixed, with gains in technology (+2.4%) and energy (+1.5%) offsetting pullbacks in utilities (-4.5%) and healthcare (-2.8%). Crude oil prices jumped 2.8% after OPEC agreed to leave output levels unchanged for the first quarter of 2026, but the move wasn’t enough to reverse the technical downtrend that has continued for the second half of this year. Gold and cryptocurrencies were down slightly for the week. U.S. Treasury yields rose despite employment and inflation data that strengthened the case for the Federal Reserve to lower rates this month. Bond traders may have been wary of a surge in new monthly U.S. corporate debt issuance, while the prospect of Japan raising rates later this month could renew volatility concerns over the carry trade unwind. The U.S. labor market remained a mixed picture, as private payroll data was soft, yet weekly jobless claims reached a three-year low. The ADP employment report showed a surprise loss of 32,000 jobs in November. However, historically that estimate has diverged from official government data, which won’t be released until December 16. The Chicago Fed estimated that the U.S. unemployment rate was unchanged in November at 4.4%, though that figure may rise given the elevated level of continuing jobless claims. There was positive news on the inflation front, as September’s long delayed core PCE price index was lower than expected at 0.2% MoM and 2.8% YoY. Consumer sentiment rose for the first time in five months, reflecting improved inflation expectations and more optimism in the outlook for personal finances. Americans now see one-year inflation at 4.1% and 3.2% annualized for the next five to ten years, the lowest levels since January. In other economic news, consumer spending on Black Friday was seen as eclipsing last year’s results, driven by a 9% surge in online shopping. U.S. manufacturing activity shrank again in November, with the ISM PMI index remaining in contraction territory for a ninth straight month. Services PMI was little changed at 52.6, with employment subdued and prices for inputs elevated. Overseas, China’s government and private sector PMI surveys both slipped into contraction as lackluster domestic demand persisted. Britain’s central bank announced initiatives to ease capital requirements for lenders in an effort to stimulate the economy, the first such reductions since the global financial crisis. Finally, the Bank of Japan offered its strongest hint yet that a rate hike is in the offing, causing money markets to raise the odds of a move on December 19 to near 80%.

THE WEEK AHEAD

The Federal Reserve’s interest rate decision on Wednesday takes center stage this week, and it may be one of the most contentious meetings in years. While fed funds futures are pricing in a near-90% likelihood of a 25-basis point cut to the 3.50%-3.75% range, there is significant division among policymakers as to the Fed’s path ahead. Five of the twelve FOMC voting members have voiced skepticism over further easing due to elevated inflation, while three members of the influential Board of Governors favor a cut. This meeting will also feature an updated Summary of Economic Projections and “dot plot” of long-range rate estimates. Financial markets may be underpricing the risk of the FOMC keeping rates unchanged, which could throw cold water on the recent rally in risk assets and trigger heightened volatility if there is a pause. There is also the specter of a potential “shadow Fed Chair” situation influencing monetary policy if the White House announces Powell’s replacement soon. U.S. economic data releases are sparse this week, with the delayed September JOLTS job openings report expected on Tuesday followed by 10- and 30-year Treasury auctions later in the week. Oracle and Broadcom, major players in the artificial intelligence space, report earnings this week. On the international side there are two central bank meetings to consider. Market participants anticipate the Reserve Bank of Australia will hold rates at 3.60% after recent GDP and inflation numbers indicated that the county’s economy is running too hot to consider a cut anytime soon. The Bank of Canada is expected to keep rates flat at 2.25% as last week’s employment data suggested a resilient labor market despite the impact of U.S. tariffs. China’s inflation and trade balance figures round out the overseas agenda.

CHART OF THE WEEK

Keep on trucking

The Dow Jones Transportation index ($DJT) rallied 3.5% last week, driven by a combination of macroeconomic data and analyst upgrades from key index components. This interest-rate sensitive sector is benefitting from the Fed’s next expected move in monetary policy. That isn’t the only catalyst though, as several of the key stocks in the index gained momentum on stabilizing shipment volumes and easing fuel costs. That data contributed to analyst upgrades for Old Dominion Freight and JB Hunt. Although new highs are still yet to be seen, last week $DJT broke above $16,500, a significant level of technical resistance for the past four years. In technical analysis, Dow Theory states that a bull market is confirmed when both the industrials index ($DJI) and transports reach new highs. Industrials have already attained that status, while the transports are now within striking distance of the record closing high from November 2024.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.