Weekly Newsletter December 29th to January 2nd

RECAPPING LAST WEEK

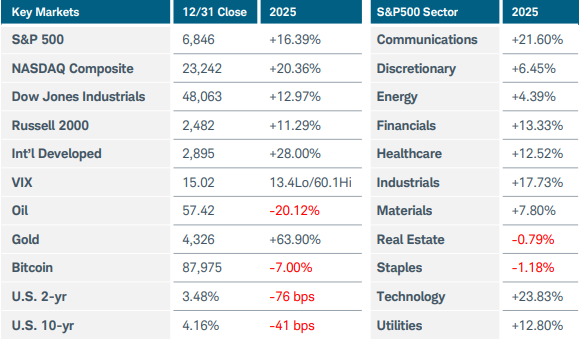

Despite ending on a four-day losing streak, the S&P500 index posted its third consecutive year of above-average returns, rising 16.4% in 2025. The U.S. equity benchmark closed the year within about 1% of its all-time high. The Nasdaq Composite gained 20.4% while the Russell 2000 rose 11.3%. International equities had the strongest performance, with the MSCI EAFE index climbing nearly 28% and the MSCI Emerging Markets jumping over 30%. Volatility as measured by the VIX ended near the lows of the year after spiking above 60 during April’s tariff-induced equity market swoon. Technology and communications were the dominant U.S. sectors, each rising more than 20%. The “Magnificent Seven” tech stocks outperformed, fueled by the allure of artificial intelligence, although some valuation concerns crept in towards year-end given those companies’ massive capex outlays. U.S. Treasury yields trended lower after peaking early in the year while the spread between short-term and long-term rates increased meaningfully. The yield on two-year notes fell 76 basis points to under 3.5% as investors priced in rate cuts from the Federal Reserve. Meanwhile, the 10-year yield finished above 4.15% as GDP growth was solid and inflation expectations remained elevated. In the commodities space, gold and silver rocketed higher, posting their best returns since 1979. Oil prices, however, suffered their worst drawdown since 2020 as multiple threats of supply disruption failed to materialize. Bitcoin’s rollercoaster year ended with the largest cryptocurrency down 7%. A sharp drawdown ensued after prices reached a record high above $127,000 in early October. Turning to year-end economic data, the long-delayed U.S. Q3 GDP data came in at 4.3% growth, well above expectations and surpassing the 3.8% rate from Q2. Consumer spending increased at a robust 3.5% rate while the PCE price index rose 2.8%, still significantly above the Fed’s 2% target. The Congressional Budget Office estimated that the government shutdown could slice one to two percentage points off Q4 GDP but that most of the drop may be recovered in subsequent quarters. U.S. consumer confidence fell for a fifth straight month in December to 89.1 on more pessimistic views of the jobs market. Minutes from the recent FOMC meeting reflected a deeply nuanced debate about U.S. economic risks, with most members ultimately supporting a rate cut given the slowdown in job creation. Overseas, China’s blue-chip CSI300 index gained 18%, its best performance in five years, despite the tariff battles with the U.S. The country’s factory activity ended the year on a positive note, with manufacturing PMI rising to 50.1 in December on a jump in pre-holiday production. President Xi pledged “more proactive” macro policies in 2026 to expand investment and support growth.

THE WEEK AHEAD

The new year got off to an inauspicious start on Friday as risk assets initially rallied but faded sharply into midday before clawing back some losses. Investors have much to consider this month as we could see a Supreme Court decision on the legality of tariffs along with the choice of a new Fed chair. Additionally, the unprecedented events in Venezuela over the weekend and the upcoming corporate earnings season may lift volatility from its year-end lows. This week’s economic calendar will be busy as the release of U.S. data starts to normalize. Top of mind will be Friday’s employment report, with forecasts calling for 55,000 jobs created in December. There may be significant revisions to the prior month’s figure of 64,000 given the low participation rate in that data batch collection. The JOLTS job openings, ADP private payrolls, and Challenger job cuts reports should provide added color on the labor market. The ISM PMI surveys will also be released this week, along with factory orders, trade balance figures, and delayed housing data. January’s preliminary consumer sentiment and inflation expectations round out the domestic agenda. On the international side, inflation updates from Europe, Australia, and China are the main releases of note.

CHART OF THE WEEK

Dollar looms large

It was a tale of two halves in 2025. The first half was marked by a sharp decline in risk assets after the U.S. announced sweeping tariffs in early April. However, a quick recovery set the stage for a strong second-half rally that left global equity indices near record highs as the year ended. Last year’s performance across different asset classes could be attributed at least in part to the U.S. dollar’s struggles. Many analysts expected the dollar to rise, as a country’s currency often benefits from higher tariffs, but instead the greenback posted its worst first half since floating exchange rates began in the early 1970s. Concerns mounted over shifts in U.S. trade and other policies while the Fed’s independence came into question. That started rumblings of a loss in confidence in traditional safe-haven assets like U.S. Treasuries, which caused a temporary rise in long-term yields that eventually subsided after the Fed resumed its rate-cutting cycle in September. Rotation away from U.S. dollar-denominated assets was evident, however, when looking at the leaders of 2025. International stocks had the best outperformance versus U.S. stocks since 2009, while international bonds also delivered outsized returns. Commodities like gold, silver, and copper soared, aided by strong demand, a weaker dollar, and falling interest rates. The U.S. dollar index ($DXY) and the 10-year Treasury yield spent much of the second half in a basing pattern amid economic uncertainty and evolving Fed policy. If Europe's growth revival materializes and the Bank of Japan becomes more aggressive raising rates, the dollar may come under renewed pressure and thus extend the positive trends of other assets like equities and commodities.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.