Weekly Newsletter December 8th to December 12th

RECAPPING LAST WEEK

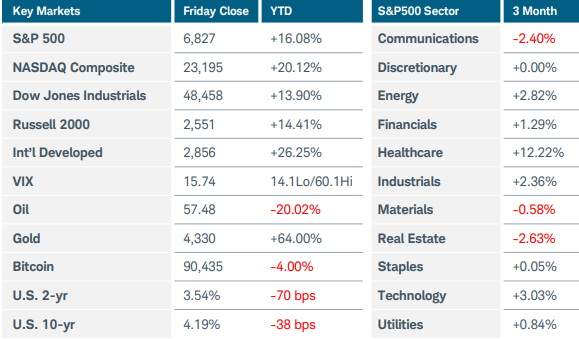

The Federal Reserve lowered its benchmark interest rate by 25 basis points while signaling a pause in further reductions as they look for clearer signals on inflation and the labor market. U.S. equity indices delivered mixed performance that culminated in Friday’s sharp selloff. Equal weight, small cap, and value indices outperformed, indicating a rotation away from large-cap growth stocks. The Russell 2000 index rose 1.2% while the Nasdaq Composite fell 1.6% and the S&P500 slid 0.6%. Basic materials were the standout sector, rising 2.4% as the metals and mining subsector jumped. Precious metals rallied sharply, with silver rocketing higher by more than 10% before giving up nearly half the gains on Friday, while gold rose 2.4%, nearing its record high from October. Technology fell 2% after earnings reports from Oracle and Broadcom renewed concerns over artificial intelligence capital outlays. The U.S. Treasury yield curve steepened after the Fed decision, with the two-year yield inching lower while the 10-year rose to near 4.2% on expectations for firmer growth and steady inflation. The division within the FOMC was apparent as two members dissented in favor of keeping rates unchanged, while a total of six had indicated no cut according to the “dot plots”. The Fed’s median outlook sees just one quarter-point cut in 2026, but with a wide dispersion of views. In its Summary of Economic Projections, the Fed saw longer term rates remaining higher than expected and bumped its 2026 GDP growth estimate up to 2.3% from 1.8%. Projections for inflation were revised lower but expected to remain above the Fed’s 2% target for several years. The Fed also announced it would begin buying Treasury bills to help steady short-term funding markets. In other economic news, the delayed JOLTS report—a combination of September and October’s numbers—showed an increase in both job openings and layoffs. The Employment Cost Index for Q3 was little changed, suggesting that labor costs are not contributing to inflation risks, though tariff-related price pressures remained elevated. On the international side, oil prices tumbled even as geopolitical tensions escalated with the U.S. seizure of a Venezuelan tanker. Prospects of a global supply surplus outweighed concerns of disruption from a sanctioned exporter. The Reserve Bank of Australia essentially ended its easing cycle, holding rates steady for a third straight meeting and stating that price risks have “tilted to the upside”. The Bank of Canada also kept its policy rate unchanged as inflation hovered near the 2% target and the country’s economic growth has proved resilient despite U.S. trade measures. Finally, higher food prices pushed China’s CPI to a 21-month high, but a continued fall in producer prices suggested that overall domestic demand remained weak. With a month still remaining in the year, China became the first country to reach an annual accumulated trade surplus of $1 trillion. Despite exports to America falling by nearly 20% due to tariffs, China continued to sell three times as much to the U.S. as it buys. Sales to other countries have ramped up considerably, leading to the record surplus.

THE WEEK AHEAD

This is the last full trading week of the year, and it is paired with a crowded agenda that includes more central bank meetings and long-delayed U.S. jobs and inflation data. Tuesday’s non-farm payrolls report will include the past two months’ data and expectations are for a significant decline from September’s 119,000 increase, although economists do not anticipate job losses as were seen in the most recent ADP private payrolls report. The October CPI report was cancelled, so Thursday’s release will reflect November and is expected to come in at +3.0% YoY, the same pace as September. These data points could strongly influence the Fed’s thinking on monetary policy going forward, but after last week’s meeting, there is a higher speed limit for growth in the eyes of policy makers. Even though its median projection suggests only one rate cut next year, fed funds futures are currently pricing in two, with the first expected in April at the earliest. Other U.S. economic releases will include retail sales, flash manufacturing and services PMIs, and a revised consumer sentiment reading. On the international calendar, the UK, Europe, and Japan have rate decisions this week. Bank of Japan Governor Ueda’s recent comments have markets almost fully pricing in a 25-basis point hike on Thursday evening. After that, speculation will turn to how the bank may proceed in 2026. The Bank of England is expected to cut rates by a quarter-point on Thursday after last week’s disappointing GDP numbers, while the European Central Bank is likely to stand pat as the region’s economic growth projections tilt upward. Other global releases to watch include the flash PMI results and China’s industrial production and retail sales figures.

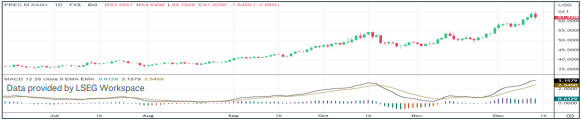

CHART OF THE WEEK

What’s driving silver prices?

Silver prices have been climbing steadily all year and accelerated above $60 per ounce for the first time last week on a rare confluence of tight supply, rising industrial demand, and accommodative monetary policy. Since most global output of silver comes from mines focused on other metals like lead, copper, or gold, increasing production is a challenge. At the same time, industrial demand has accelerated as growing sectors like electric vehicles, solar panels, and data centers are transforming silver from a precious metal to a critical one. Falling short-term interest rates and downward pressure on the U.S. dollar also tend to increase demand for non-yielding assets that are viewed as a store of value. Even though the Fed suggested that rate cuts could be on hold for a while, market watchers anticipate that the downturn in short-term yields and the dollar will continue. The current situation, with an ounce of silver now worth more than a barrel of oil, has only happened twice before but could persist given the technical trends.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.