Weekly Newsletter February 16th to February 20th

RECAPPING LAST WEEK

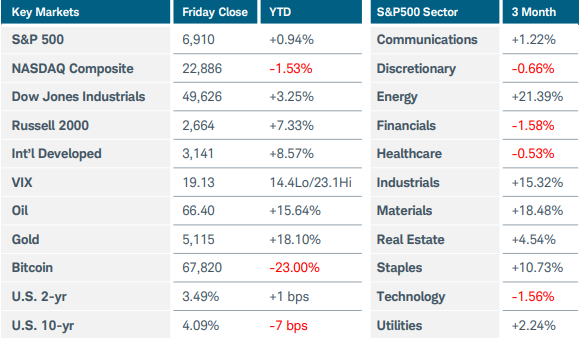

U.S. equity indices gained ground as investors sorted through a slew of economic reports while also weighing the implications of Friday’s Supreme Court decision to strike down President Trump’s sweeping tariffs. The Nasdaq Composite rose 1.5%, while the S&P500 gained 1% and Russell 2000 added 0.6%. Sector performance was split, with gains in financials, communications, and industrials offset by weakness in staples, materials, and healthcare. Private equity companies suffered losses after Blue Owl Capital’s decision to sell $1.4 billion in assets and freeze redemptions at one of its funds. The moves fueled additional worries about lenders’ exposure to certain industries like software. Shares of Walmart fell after the company issued a conservative forecast in its earnings release. In commodities, gold prices edged higher while silver jumped 9% to $84.25. U.S. Treasury yields rose after a mixed batch of economic data. The long-delayed first estimate of Q4 2025 GDP came in much lower than expected at +1.4%, decelerating sharply from the prior quarter’s growth of 4.4%. A pullback in consumer spending and exports, combined with the government shutdown, were cited as the main reasons for the weaker reading. Another delayed report showed that U.S. inflation increased more than expected in December. The Core PCE Price Index rose 0.4% MoM and 3.0% YoY. Minutes from the last FOMC meeting included the first recent mention of potential rate hikes if inflation remains above the 2% target. Policymakers remained split over their next move and fed funds futures currently reflect just over 50% chance of a quarter-point rate cut in June. In other economic news, U.S. business activity continued to expand this month, albeit at a slowing rate. The S&P Global flash Composite PMI slipped to 52.3 from 53.0, with new orders and employment stalling. The final consumer sentiment reading for February slipped to 56.6 from an initial estimate of 57.3, with one-year inflation expectations sitting at 3.4%. The U.S. trade deficit widened in December, leaving the goods shortfall in 2025 at the highest on record despite higher tariffs on foreign merchandise. Finally, pending sales of existing homes fell to a record low in January as buyers retreated despite falling mortgage rates and a slower pace of price increases. Overseas, business growth continued to outpace expectations in Europe, with Germany’s flash composite PMI rising to 53.1 this month from 52.1. The manufacturing component rose above the 50 level that represents expansion for the first time since June 2022. Britain’s inflation rate dropped to 3.0% YoY in January while employment and wage growth figures softened, strengthening the case for a rate cut in March.

THE WEEK AHEAD

The economic calendar is light this week, leaving investors with more time to ponder the potential consequences of the U.S. Supreme Court’s momentous decision on tariffs. The big questions will be whether the government must refund tariff revenue, how much might have to be paid back, and over what timeframe. The administration’s response to the ruling is a source of uncertainty, along with how the U.S. would replace the expected future revenue that could have been used to service its debt. Bond prices may come under pressure as worries resurface over government finances, which could push longer-term yields higher. The decision could also affect sectors that derive significant revenue from non-U.S. sales, as well as those sensitive to raw material and component prices. One of the most important earnings announcements of the season arrives on Wednesday after market close. Nvidia is expected to report earnings and revenue growth around 70% YoY, but investors are likely to zero in on gross margins and forward guidance. Retailer Home Depot also reports this week. On the economic calendar, Friday’s Producer Price Index will be the main release of interest, as a hot reading could weigh on rate cut expectations. Consumer confidence and factory orders are also on the docket. There are many appearances from FOMC members this week with opportunities to comment on recent developments. On the international side, inflation updates in Germany, Japan, and Australia are the releases of note.

CHART OF THE WEEK

A crude barometer

There are few better instant measures of the geopolitical climate than the price of oil. Last week, crude oil futures jumped 5.7% to $66.40 after President Trump warned Iran that an agreement on the country’s nuclear program needs to be reached in the next couple of weeks. The U.S. has deployed a massive military buildup in the Middle East, fueling fears of a wider war developing in the region which produces about a third of the world’s oil. With investors and policymakers hyper-focused on inflation, rising crude prices that lead to more expensive gasoline would be a most unwelcome development. Costs at the pump tend to feed into inflation data quickly and can have a negative impact on consumer sentiment and spending. From a technical perspective, crude oil futures have broken out of a three-week long consolidation range and appear poised to continue their intermediate-term uptrend that began in early January. The 50-day moving average is still below the 200-day but closing the gap, while the MACD indicates bullish momentum. The next technical resistance awaits near $70 with the 52-week high of $78.40 above it. For the most part, oil traders spent the past six months ignoring geopolitical threats that never materialized into actual production disruptions. We may find out soon if the current situation plays out differently.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.