Weekly Newsletter February 23rd to February 27th

RECAPPING LAST WEEK

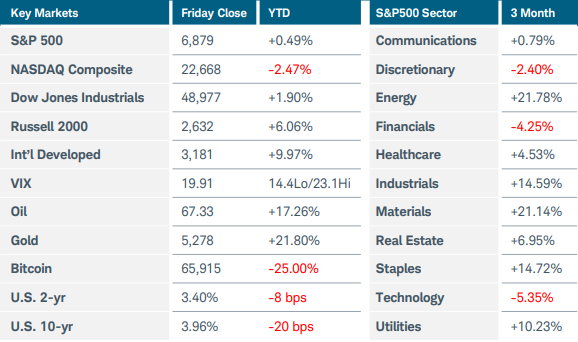

U.S. equity indices fell after a hotter-than-expected wholesale inflation report while technology stocks came under pressure following Nvidia’s earnings report. The Nasdaq Composite and Russell 2000 indices lost around 1%, reversing gains made earlier in the week. The S&P500 slid 0.5%. Sector performance tilted positive but was offset by notable weakness in financials and technology. Solid fourth-quarter results and a positive forecast from chipmaking giant Nvidia failed to excite investors—shares 6.5%, dragging down other names in the sector. Software companies continued to be negatively impacted by new tools released by artificial intelligence lab Anthropic. Gold futures rose 3% while silver jumped more than 11% to $94.40. U.S. Treasury yields continued their month-long slide, with the 10-year note falling below 4% for the first time in three months. Fresh uncertainty over U.S. trade policy and ongoing unease about AI investment pushed investors towards more defensive posturing last month, boosting bond prices and lowering interest rates. Turning to economic data, Friday’s Producer Price Index release revealed that inflation could pick up in the months ahead. PPI rose 0.5% MoM in January as margins for services companies surged, suggesting businesses were passing on tariff costs to consumers. Adding to inflation concerns was a report that rare earth metal shortages are pushing up prices for U.S. aerospace and semiconductor firms. China’s control of the rare earth market is likely to be an important topic during the upcoming meeting in Beijing between Presidents Trump and Xi. U.S. consumer confidence edged higher in February to 91.2 from 89.0 as views of labor market conditions improved slightly. On the international front, crude oil prices rose 1.5% last week amid reports that OPEC+ will likely consider raising output in April, ending a three-month pause. In Japan, the nomination of two advocates of economic stimulus to the central bank’s board sent the yen lower while the Nikkei 225 stock index soared to another record high. The move, combined with tame inflation report, may affect the Bank of Japan’s plans for raising interest rates. Australia’s CPI rose more than expected in January to 3.4% YoY, increasing odds of another rate hike this year. Germany’s consumer inflation eased to 2% last month as lower energy costs and a strong euro versus the U.S. dollar kept price increases at bay. Finally, Canada’s economy unexpectedly contracted in Q4 2025, with GDP falling 0.6% as manufacturers opted to draw down existing inventories rather than increase production. On a positive note, exports rose 1.5% despite declining trade with the U.S.

THE WEEK AHEAD

As the calendar turns to March, oil and gas prices are surging as the U.S. and Israeli assault on Iran expands across the Middle East. The air war is already impacting energy production, and interest rates and the U.S. dollar rose to begin the week as the potential for inflationary pressures emerged. AI disruption and trade policy are also likely to continue complicating the outlook for investors. Banks suffered losses late last week after the collapse of a UK mortgage provider raised wider concerns about lending standards, adding another layer of risk to consider. Recently, rate cut expectations for this year have been pared back, putting extra emphasis on this week’s U.S. employment data. ADP private payrolls and Challenger job cuts data will precede Friday’s nonfarm payrolls report, in which economists are forecasting an increase of around 60,000 jobs for February after the prior month’s surprisingly robust report. There will be an additional labor market update before the Fed’s next rate decision on March 18. Other economic reports of note this week include ISM manufacturing and services PMIs and January’s retail sales. Earnings reports to watch are Target before the opening on Tuesday and semiconductor company Broadcom on Wednesday after the bell. Overseas, China’s latest batch of PMI data arrives on Tuesday evening, along with Australia’s Q4 2025 GDP. In Europe, investors have CPI, PPI, and retail sales data to sort through, as well as accounts from the last central bank meeting.

CHART OF THE WEEK

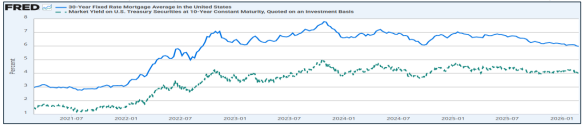

Mortgage rate relief?

Last week the average rate on the 30-year fixed-rate mortgage (blue line) fell below 6% for the first time since September 2022. That rate tends to track with the 10-year U.S. Treasury yield (green line), which sank throughout February as investors sought stability in the fixed income markets due to higher volatility in equities and uncertainty triggered by the Supreme Court’s tariff decision. Too few affordable homes that could appeal to first time buyers, as well as a generally low level of available inventory, are among the biggest drags on the housing market. Although inventory levels have improved, many homeowners are still reluctant to sell due to having current mortgages under 5%. There have also been reported increases in homeowners taking their houses off the market due to lower prices. National home prices grew only 1.3% in 2025, the weakest gain since 2011, and well below the average 6.6% annual gain seen over the past 10 years. New construction continues to be hampered by land regulations, uneven labor supply, and higher building material costs. Mortgage rates dipping below 6% could be an important psychological motivation for buyers. Still, it remains to be seen whether other factors, such as the government’s plan to buy mortgage bonds, will have the desired impact on affordability. And further rate declines may be hampered by stubborn inflation and concerns about U.S. fiscal sustainability.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.