Weekly Newsletter February 2nd to February 6th

RECAPPING LAST WEEK

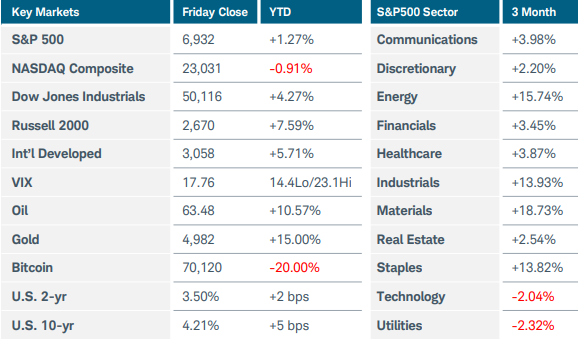

A sharp three-day selloff hit risk assets as investors reassessed some of the potential economic impacts from artificial intelligence adoption. The Nasdaq Composite index bounced back more than 2% on Friday but still ended the week lower by 1.8%, while the S&P500 was flat. Smaller companies and equal-weight indices continued to outperform as the S&P400 MidCap 400 jumped 4.4%, and the Russell 2000 and the S&P500 Equal Weight each gained more than 2%. Sector performance favored cyclicals like basic materials (+4.5%), energy (+4.3%), and industrials (+4.7%), while consumer staples soared 5% after Pepsico and Colgate-Palmolive saw positive reactions to their earnings reports. Technology slid 2% and the software sub-index plunged 9% after Anthropic unveiled an AI tool viewed as a potential replacement for widely used software products in the legal and finance fields. Shares of Advanced Micro Devices sank midweek after delivering a lackluster sales forecast, while Amazon tumbled on Friday after forecasting $200 billion in capital expenditures this year, a 50% increase YoY. Precious metals remained highly volatile, with silver sinking to $63.90 and ultimately ending the week lower by 9% at $77. Gold finished with a small gain after trading in a wide range. Fears of another “crypto winter” added to investors’ anxiety after Bitcoin cratered by 30% to $60,000 before recovering about one-third of the losses on Friday. Turning to economic news, the partial U.S. government shutdown ended on Tuesday, and though it was brief, it pushed the release of January’s non-farm payrolls report to February 11. Other data reflected a labor market that continues to soften. Private payrolls increased by just 22,000 in January and wage growth slowed. Job openings in December fell to the lowest level since 2020 while layoffs jumped above 100,000 last month. However, Amazon and UPS accounted for most of the cuts, and although weekly jobless claims increased more than expected in the last week of January, the underlying trend remained stable. U.S. Treasury yields fell in reaction to the weaker jobs data while bond prices also caught a bid from investors seeking shelter from volatility in risk assets. ISM Manufacturing PMI moved into expansion territory for the first time in a year, but survey respondents were still wary of tariffs and rising raw material prices. Consumer sentiment improved at the start of February as one-year inflation expectations plummeted half a percentage point to 3.5%, the lowest level since January 2025. Overseas, OPEC kept oil output unchanged for March amid Middle East tensions. Crude oil futures fell 3.4% in volatile trading as news of talks to de-escalate friction between the U.S. and Iran were weighed against incidents in the Strait of Hormuz. The European Central Bank left rates unchanged and offered no insight into its next move. Inflation in the Eurozone dipped to 1.7% YoY in January while core CPI edged down to 2.2%. The Bank of England also kept rates on hold in a closer than expected vote, suggesting differing opinions on how much evidence is needed that inflation is trending lower. The Reserve Bank of Australia became the first to raise rates this year, citing persistent inflation pressures and a stronger economy running up against capacity constraints.

THE WEEK AHEAD

The volatility index (VIX) jumped to 23 last week before calming down on Friday and settling below 18. The price action demonstrated how quickly short-term sentiment can shift when it comes to themes like AI. Volatility seems likely to persist as investors attempt to sort through who will be the winners and losers in a technology that many see as transformative. How and when that happens and what disruptions occur along the way are still big unknowns. This week, the delayed U.S. jobs report and Friday’s CPI release take center stage. Price pressures have become more evident in recent PPI and PMI reports, so economists will be eager to see if higher costs are being passed on to consumers. Retail sales from December will be released as that dataset is still playing catch-up from last year’s government shutdown. Other events of note include 10- and 30- year Treasury auctions. Earnings season is winding down, but given the recent carnage in technology stocks, reports from software companies AppLovin and DataDog along with networking giant Cisco Systems will garner attention. Overseas, Prime Minister Takaichi is expected to secure a solid win for her ruling majority in Japan’s lower house elections over the weekend. Preliminary GDP estimates for Q4 will be release in the UK and Eurozone. China’s monthly inflation update rounds out the international calendar.

CHART OF THE WEEK

A bit of a retreat

Anytime an outsized move occurs in an asset’s price it can be useful to consider the technical picture and look for signs of exhaustion or capitulation. This year, there has been some evidence of investors shifting to more of a “risk-off” approach which has affected the various asset classes in different ways. While there wasn’t any specific news that triggered the sharp selloff in Bitcoin and other cryptocurrencies last week, a numbers of factors have been in play since prices peaked in October. The “Magnificent 7” technology stocks topped around the same time, as concerns over future Fed policy, the potential for tighter financial conditions, extended stock valuations, and the possibility of a bubble in AI investment hit many risk assets. For Bitcoin, the persistent downtrend triggered liquidations in leveraged positions along with outflows from exchange-traded products. The world’s largest cryptocurrency has seen extreme volatility throughout its history, and the chart reveals a wide downward channel that has formed since last fall’s highs. The drop’s acceleration last week and Friday’s recovery may be viewed as initial signs of capitulation. While any kind of trend reversal is a long ways off, investors will be watching how Bitcoin reacts to this potential support level at the channel bottom. Major technical resistance lurks above, near $84,000.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.