Weekly Newsletter January 12th to January 16th

RECAPPING LAST WEEK

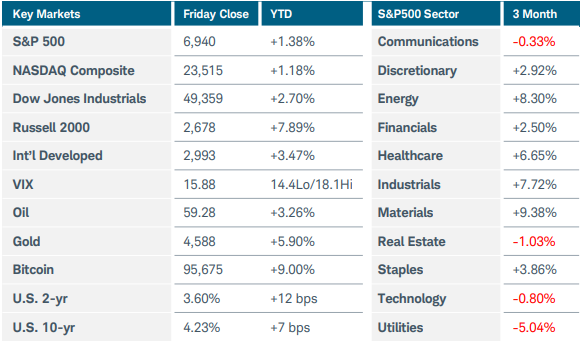

Investors’ attention turned to U.S. corporate earnings reports amid geopolitical turbulence and friction between the Justice Department and Federal Reserve. The S&P500 and Nasdaq Composite indices ended the week slightly lower, while the Russell 2000 rose 2% and the S&P Midcap 400 gained 1.3%. The outperformance of smaller companies along with equal-weight indices continued to highlight the rotation away from large caps that has been evident early in 2026. At the sector level, consumer staples jumped more than 3.5%, maintaining a strong start to the year. Financials fell more than 2% as talk of capping credit card rates and mixed earnings reports from U.S. banks weighed on the sector. Large money-center banks like JP Morgan Chase and Citigroup exceeded analysts’ earnings estimates on strong lending demand. However, they missed revenue expectations in areas like investment banking, which in turn boosted profits for historically dominant players Goldman Sachs and Morgan Stanley. In commodities, gold reached a new record high above $4,650, while silver soared more than 17% to $93.70 before pulling back at week’s end. Fears of a U.S. strike on Iran to quell the unrest there subsided, causing crude oil to fall more than 4% on Thursday, though it held onto modest gains for the week. U.S. Treasury yields ticked higher after economic data did little to change expectations regarding the Fed’s next rate cut. Consumer prices increased in line with forecasts last month, with CPI rising 0.3% MoM and 2.7% YoY. November’s delayed retail sales report advanced 0.6%, pointing to solid economic growth in Q4 2025. Renewed concerns over the Fed’s independence likely also contributed to the rise in yields after the U.S. Department of Justice threatened a criminal indictment of Chair Powell. In other economic news, existing home sales jumped 5% in December while delayed data showed that new home prices continued to drop at the end of last year on weak demand and high inventory. On the international side, the Japanese yen fell to multi-year lows against the U.S. dollar and the euro before rebounding slightly to end the week. Prime Minister Takaichi said she will call a snap election later this month in an effort to secure a mandate for the new ruling coalition. The move may allow her to advance plans for a pro-stimulus economic agenda, which may lift Japanese stocks but would likely send bond yields higher and the keep downward pressure on the yen. China’s 2025 trade surplus surged to nearly $1.2 trillion, up from $992 billion the year prior. Increased shipments to South America, Southeast Asia, Africa, and Europe largely offset the sharp drop in exports to the U.S. Finally, UK GDP grew by a better-than-expected 0.3% in November, lifting hopes for economic improvement this year backed by more rate cuts.

THE WEEK AHEAD

A shortened week awaits following Monday’s holiday for Martin Luther King Jr. Day. Despite all the geopolitical and domestic political issues that loom large, investors have mostly stayed the course thus far, focusing on generally positive economic data. Volatility has risen from its lows but overall remains subdued. For the rest of this month, corporate earnings reports will likely be an important driver of the news cycle. This week, attention will shift from the banks to a more diverse set of companies, including Netflix, Intel, Proctor & Gamble, Johnson & Johnson, Freeport-McMoRan, DR Horton, and others. On the U.S. economic calendar, the delayed PCE Price Index data from October and November will be released Thursday, along with the final reading of Q3 GDP. Then on Friday comes the S&P Global flash PMI readings for the U.S. and other developed economies. Additionally, at week’s end the Bank of Japan is expected to leave interest rates unchanged, even as the yen remains under pressure. No further hikes are anticipated until this summer, and the Japanese government may be forced to intervene at some point to support its flagging currency. The World Economic Forum gets underway this week in the Swiss alpine town of Davos, where leaders will gather to discuss challenges confronting the global economy. The international economic calendar features China’s GDP, industrial production, and retail sales figures, as well as inflation updates from Canada and the UK.

CHART OF THE WEEK

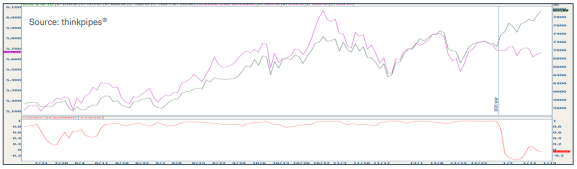

Semi-charmed kind of life

Typically, the PHLX Semiconductor Index (SOX) is highly correlated with the overall technology sector, as its component stocks make up over 40% of the broader S&P500 Information Technology Index ($SP500#45). This week’s chart shows the 10-day correlation between the two indices, which had been above 80% from last August through year-end. Things have changed dramatically in 2026. Earnings reports from semiconductors have greatly exceeded expectations and forward guidance has been strong, with Micron Technology one of the recent standouts. Taiwan Semiconductor is the latest example, with the world’s largest contract chipmaker reporting blowout earnings last week amid news that the U.S. and Taiwan had struck a trade deal favoring more mutual technology investment. The broader tech index is dominated by giants like Apple, Microsoft, and Meta Platforms, which are not part of the SOX index. Thus, the sharp divergence in performance as the mega-caps have fallen behind to start the year. With some investors considering diversifying away from the big winners of the past several years, mega-caps may continue to lag. Small to mid-size semiconductor company performance is also contributing to the widening gap between SOX and the tech sector index.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.