Weekly Newsletter January 19th to January 23rd

RECAPPING LAST WEEK

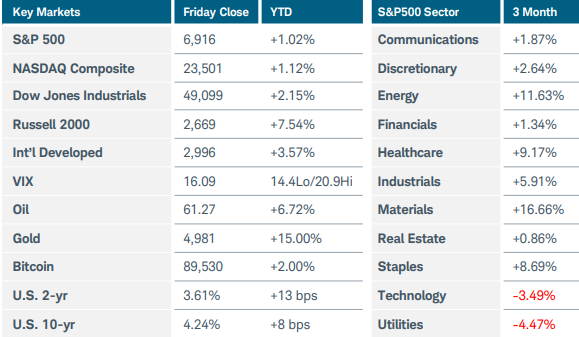

U.S. equity indices ended with mixed performance after a turbulent week in which President Trump’s pursuit of Greenland threatened to upend trade relationships. After opening the shortened trading week with a sharp 2% drop, the S&P500, Nasdaq Composite, and Russell 2000 indices recovered most of their losses. Although tensions between the U.S. and Europe eased somewhat by week’s end, investors’ move toward non-U.S. assets gained further momentum. The U.S. dollar suffered its worst weekly decline since June, while precious metals continued to soar. Gold, the traditional store of value in unstable times, jumped 8% to $4,980 and silver leapt 14% to break above $100 for the first time. Selling pressure in U.S. Treasuries pushed the 10-year yield up to a five-month high of 4.3% before backing off slightly. International equities have seen strong inflows in 2026, especially emerging markets which tend to benefit most from a weak dollar. U.S. sector performance was uneven, with rising oil prices supporting energy’s 3% gain while rate sensitive sectors like financials, utilities, and real estate all fell more than 2%. Technology component Intel plunged 17% after the company posted a quarterly loss and worse-than expected outlook. Turning to economic data, long-delayed core PCE price index data from November revealed a 2.8% YoY increase, only a modest uptick from the prior month. However, the recently released CPI report suggested that December’s core PCE reading—which will be released on February 20—could show a 3.1% rise YoY. U.S. business activity remained in expansion territory this month, though signals of slowing momentum emerged. The S&P Global Flash Composite PMI stood at 52.7 but job growth has stagnated while higher input costs have pushed up selling prices. The final January consumer sentiment index rose to a five-month high of 56.4 on economic optimism, though this figure is still 20% below its level a year ago. One-year inflation expectations fell only slightly to 4%. Overseas, the Bank of Japan kept rates unchanged at 0.75% while retaining its hawkish inflation and economic growth forecasts. Prior to that decision, Japanese bond yields jumped to 27-year highs after Prime Minister Takaichi pledged to cut the consumption tax rate. This move stoked fears that the country could struggle to service its debt to-GDP ratio, the highest among developed economies, and thus its financial stability. In China, GDP growth met the government's 5% target last year largely by snatching a record share of demand for global goods, a strategy seen by many economists as unsustainable in the long run. Domestic consumption continued to weaken as the year went on. Finally, Eurozone business activity was stable at 51.5 this month, while UK inflation rose to 3.4% YoY in December but was not expected to derail rate cuts anticipated for later this year.

THE WEEK AHEAD

The shifting geopolitical landscape’s effect on sentiment was evident last week, reviving talk of the “Sell America” trade that emerged after last April’s sweeping tariffs announcement. Investors await more details on negotiations between the U.S. and NATO regarding Greenland while also looking to corporate earnings and the Federal Reserve meeting. The Fed is widely expected to keep rates steady when it announces its policy decision on Wednesday, but questions around the central bank’s independence may be more top-of-mind for this meeting. The busiest week of this corporate earnings season provides investors with an opportunity to see how artificial intelligence-related investment is progressing. Quarterly updates from Apple, Meta Platforms, Microsoft, Tesla, UPS, Boeing, Chevron, and many more are on the docket. The U.S. economic calendar includes consumer confidence, durable goods and factory orders, and the producer price index. The Bank of Canada is also expected to keep rates unchanged this week, as the country’s economy is holding up reasonably well in the face of U.S. tariffs. In Europe, the first estimate of Q4 GDP arrives Friday along with Germany’s December CPI. Inflation updates from Japan and Australia are also on the international calendar. Odds are rising that the Bank of Australia may raise rates at its meeting next month with inflation on the rise, while an extension of recent declines in Japan’s CPI may put additional pressure on the yen.

CHART OF THE WEEK

Steepening curves

While short-term interest rates are heavily influenced by Fed policy, longer-term rates are much more impacted by market expectations for economic growth, inflation, and other factors. Many Americans would like to see long-term rates come down to help with issues like housing affordability. It has been an uphill battle, and last week’s tariff threats pushed longer-term Treasury yields noticeably higher. The chart below shows the 10-year Treasury Rate index (TNX:CGI) along with the yield spread between 10-year notes and three-month bills (purple line). The yield curve steepening accelerated last month as traders priced in two rate cuts for 2026, which has sent short-term rates lower. Meanwhile, the long end is rising due to geopolitical shifts and concerns about fiscal sustainability, in addition to higher growth and inflation forecasts. Bond investors must also consider the impact from events like last week’s flareup in Davos regarding tensions over Greenland. Bond vigilantes continue to discuss the potential for a mass exodus from U.S. debt, though this has yet to materialize. Instability in global bond markets has been on the rise over the past year, with Japan the latest example from last week. A continued steepening of the Treasury yield curve could put additional pressure on U.S. assets.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.