Weekly Newsletter January 5th to January 9th

RECAPPING LAST WEEK

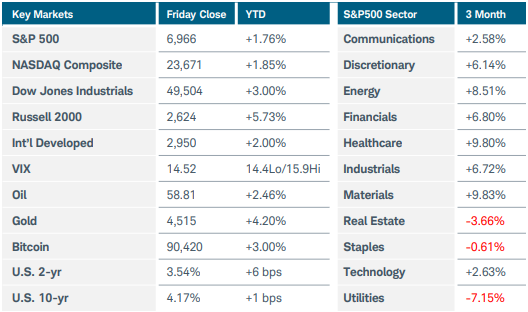

U.S. equity indices completed the first full week of 2026 in positive territory as investors reacted to softer-than-expected labor market data. The S&P500 and Nasdaq Composite indices each gained more than 1.5% while equal-weight and value themes continued to outperform. The Russell 2000 jumped 4.6% on hopes for rate cuts and a strong showing from financial stocks. For S&P500 sectors, consumer discretionary rallied 5% as retailers soared, while basic materials saw nearly similar gains as precious metals once again approached record highs. Gold futures rose 4% and silver spiked more than 10% in extremely volatile trading. OPEC’s decision to leave oil output levels unchanged at a brief meeting last weekend was supportive of crude, which finished the week higher by 2.5%. U.S. Treasury yields fell after December’s non-farm payroll growth came in below expectations at 50,000. At the same time, the unemployment rate ticked lower to 4.4% despite a rise in layoffs attributed mostly to federal government workers and technology companies. Overall, the data suggested that labor demand continued to fade without rapid deterioration, even as economic growth appeared robust. Fed funds futures still project two rate cuts in 2026, although the first isn’t being priced in until June. In other economic news, ISM manufacturing PMI slumped to 47.9 in December, while services PMI rose to 54.4, its highest level since October 2024. Tariff impacts were common themes among survey respondents as the price indices remained elevated. This month’s preliminary consumer sentiment index improved slightly but still sat near record lows. One-year inflation expectations were flat at 4.2% while the long-term view edged up to 3.4%. Delayed U.S. trade data revealed a deficit of just $29.4 billion in October, down 39% from the prior month and the lowest level since 2009. The declining imbalance could provide a much-needed boost to Q4 GDP, considering the expected negative impact from the government shutdown. Another long-delayed report showed that U.S. worker productivity grew sharply in Q3 as business investment in artificial intelligence depressed labor costs. Overseas, inflation in Germany and the wider Eurozone slowed to 2% YoY last month, rekindling hopes that the European Central Bank could resume rate cuts this year. German retail sales fell 0.6% MoM, a sharp reversal from prior readings that raised concerns about consumer spending. China’s CPI accelerated at the fastest pace in nearly three years, largely driven by supply shortages of hard-to-obtain foods during the cold winter. However, producer prices continued their deflationary streak, indicating soft domestic demand for goods.

THE WEEK AHEAD

Several interesting developments arose last week that could have a major impact on the economy’s direction in 2026. The first was in the housing market, where the U.S. government may move to buy mortgage bonds to bring down homebuyer costs while also banning investment firms from buying single-family homes. Second, the U.S. government is expected to request a 50% increase in the defense budget, to $1.5 trillion, and may look to tie defense companies’ dividends, share buybacks, and executive pay to delivery schedules. Meanwhile, the White House stepped up its pressure on the Federal Reserve over the weekend, while the U.S. Supreme Court is expected to issue its next rulings on Wednesday, which could include the legality of President Trump’s sweeping global tariffs. The flurry of news may introduce some caution among investors, despite the overall positive start to markets this year. On this week’s economic agenda, Tuesday’s U.S. CPI report will take center stage, flanked by other releases including retail sales, housing data, regional manufacturing surveys, and Treasury auctions at the longer end of the curve. Earnings season also gets underway on Tuesday, with reports from the major U.S. banks sprinkled throughout the week along with technology giant Taiwan Semiconductor. The international calendar is light, highlighted by China’s trade balance figures and the UK’s monthly GDP update.

CHART OF THE WEEK

Latin emergence

The outperformance of international equities versus the U.S. was a major theme of 2025. The strongest subset was Latin America, represented here by the FTSE Emerging Latin America Index (AG02:FTSE). It outpaced the rest of the globe throughout 2025, partly because a 30% decline the year prior meant it started the year with depressed valuations. The index recovered that entire move and last week rose to highs not seen in nearly four years. Easing inflation and stable monetary policy from several countries in the region boosted corporate earnings and investor risk appetite, while the weak U.S. dollar strengthened local currencies. This amplified returns for foreign investors. A broader shift toward more market-friendly governance also boosted confidence, capped off by the removal of Nicolas Maduro in Venezuela. That was a pleasant surprise for Venezuelan equities and sovereign debt as investors hope the country will reintegrate with global markets after years of sanctions and economic isolation. However, U.S. intervention does introduce heightened geopolitical uncertainty, including potential for diplomatic friction from regional governments. Volatility may increase as policy and leadership restructuring unfold. Relations between Venezuela and the U.S. may ultimately improve, but how that develops is still up in the air, especially pertaining to the South American country’s vast oil reserves. If this hoped for stability arrives, Latin American markets could see further gains in 2026.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.