Weekly Newsletter July 14th to July 18th

RECAPPING LAST WEEK

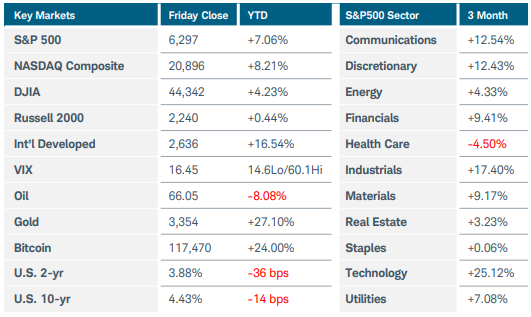

Major U.S. equity indices ascended to a fresh weekly closing high as signs of economic strength and positive corporate earnings reports overshadowed the increased pressure from the White House on Federal Reserve Chair Powell. The Nasdaq Composite gained 1.5%, while the S&P500 and Russell 2000 added less than 1%. S&P500 sector performance was mixed; technology jumped 2% after key supplier Taiwan Semiconductor reported strong Q2 earnings, while energy slid 3.5% along with crude oil prices. Financials advanced after the large U.S. banks posted Q2 profits that jumped more than 20% YoY. In crypto news, the U.S. House passed the Genius Act, a bill creating a stablecoin regulatory framework, along with two other bills that could lead to wider adoption of digital assets. Bitcoin prices ended up slightly lower for the week, but Ethereum soared nearly 20% as inflows to exchange-traded products that track the second-largest digital currency spiked to record highs. U.S. Treasury yields began to climb following Tuesday’s CPI report which revealed an uptick in consumer prices for June. Higher food and energy prices pushed CPI up by 0.3% MoM and 2.7% YoY, largely in-line with forecasts. Shelter, vehicle, and travel-related costs moderated but several categories felt the effects of tariff increases, including furnishings, audio-video products, and appliances. Longer-term Treasury yields jumped midweek, and the dollar plunged after reports emerged that President Trump was strongly considering replacing Fed Chair Powell. Although stocks pared losses after the President said the move was “highly unlikely”, investors may remain cautious given the administration’s increasing pressure to lower rates—an improbable outcome of the next FOMC meeting. In other economic news, U.S. retail sales rebounded last month, although these figures are not adjusted for inflation. Consumer sentiment lifted to 61.8 from 60.7 this month, buoyed by an improving economic outlook and softening inflation expectations. Americans expect prices to rise by 4.4% over the next year, down from 5%. Manufacturing activity expanded in the New York and Philadelphia regions while price pressures remained elevated. The housing sector continued to suffer from high mortgage rates with single-family starts and permits falling sharply in June. The supply of new homes rose to levels last seen in late 2007. Overseas, China’s economy grew 5.2% YoY in Q2, slowing from 5.4% in the prior quarter. Industrial production accelerated 6.8% YoY in June, while retail sales growth eased to 4.8% from 6.4%. Property investment sagged despite multiple rounds of stimulus support and new home prices tumbled last month. China ended the first half of 2025 with a record trade surplus as firms were able to increase sales to other markets to compensate for reduced U.S. trade. UK CPI unexpectedly ticked up to 3.6% in June, the highest rate for any advanced economy. Economists still expect the Bank of England to cut rates next month as the labor market has continued to cool.

THE WEEK AHEAD

Global economies continue to hum along despite the constant barrage of trade tensions and geopolitical conflicts. This week’s release of flash PMI data will provide an update on the economic environment for developed nations in the face of ongoing uncertainty. In the U.S., investors will also focus on data such as new and existing home sales, along with durable goods orders. A number of notable companies report earnings this week, including Alphabet, Tesla, Intel, IBM, Texas Instruments, General Motors, Coca-Cola, and Capital One Financial. Fed Chair Powell is scheduled to speak at a conference on Tuesday morning. While the U.S. dollar has recovered in recent weeks, last week’s events demonstrate that pressure from Washington is mounting on the central bank and the greenback. Overseas, the European Central Bank is expected to keep rates unchanged on Thursday, with just one more cut forecasted by year end. Japan’s Upper House Parliamentary elections over this past weekend may affect their central bank’s plans to raise interest rates. Surveys suggest that Prime Minister Ishiba’s coalition may lose its majority, giving opposition groups traction to pressure the BOJ into keeping rates low to ease the impact from the country’s enormous debt burden. The rest of the international calendar includes minutes from the recent Reserve Bank of Australia meeting, Japan’s core CPI reading, and British retail sales.

CHART OF THE WEEK

Powering forward

The relentless ascent of equity indices has been driven largely by the technology sector, which is increasingly dependent on additional power sources. Goldman Sachs projects global data center electricity demand will increase by 50% by 2027 and 165% by 2030. Recently, Meta Platforms announced plans to build two artificial intelligence (AI) clusters which are expected to use six gigawatts of power annually—six times the annual power used by all the homes in Denver. Other tech companies are setting up similar facilities. This enormous anticipated demand is also a reason to modernize existing infrastructure and expand clean energy aspects. With equities at all-time highs, some investors may be interested in diversifying into historically lower-volatility, higher yielding sectors that could still participate in the AI revolution. Utilities is one sector that could benefit from such a rotation. From a technical perspective, the utilities sector index ($SP500#55) finally broke above the $420 resistance area last week, pulling the RSI indicator to a bullish position near 65. Utility companies generally run higher debt levels than other sectors due to the capital-intensive nature of the business, so the prospect of lower interest rates later this year could be an additional tailwind.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.