Weekly Newsletter July 21st to July 25th

RECAPPING LAST WEEK

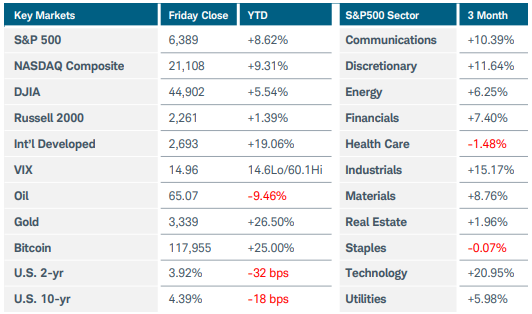

The S&P500 and Nasdaq Composite continued their push into record-high territory, rising 1.5% and 1%, respectively. Positive momentum from corporate earnings reports and trade negotiations outweighed ongoing tensions between the White House and Federal Reserve. The Russell 2000 rose nearly 1%, while international developed markets outperformed the U.S. All eleven S&P500 sectors gained ground, led by a 3.5% jump in healthcare. Crude oil and gold prices fell, while Bitcoin was flat and Ethereum rose another 5%. U.S. Treasury yields eased slightly with the 10- year note settling near 4.4% ahead of the Fed’s next decision on rates. Mixed signals on the tenure of FOMC Chair Powell persisted after President Trump visited the Fed’s headquarters on Thursday. On the trade front, a deal with Japan was announced that purports to lower tariffs on auto imports, while the European Union was optimistic that an agreement with the U.S. could be reached before the August 1 deadline. Turning to economic data, weekly jobless claims totaled just 217,000 as the U.S. labor market remained on solid footing. Domestic business activity accelerated this month, but companies sought higher prices for goods and services and remained concerned about tariffs and government policy changes. The S&P Global flash composite PMI index rose to 54.6, boosted by a surge from the services sector. The prices paid index edged up to 61.9 from 61.2, while the price gauge for services inputs jumped to 61.4 from 59.7. The housing market continued to struggle under the weight of high mortgage rates. Existing home sales fell 2.7% last month as supply jumped 16% YoY. The median sales price reached $435,300, a record for the month of June and the 24th straight month of annual gains. The inventory of new U.S. single-family homes rose to levels not seen since 2007, forcing builders to cut prices to attract buyers. Overseas, Japan’s Prime Minister Ishiba vowed to remain party leader despite losing control of the upper house in Sunday’s election. The upheaval may convince the Bank of Japan to reconsider its plans for raising interest rates. Inflation pressures eased slightly but remain above the BOJ’s 2% target. The European Central Bank left rates unchanged, and its modestly positive economic assessment suggested that future rate cuts may not be in the offing. Eurozone flash PMIs reflected marginal growth this month.

THE WEEK AHEAD

This week is shaping up to potentially be one of the most pivotal of the year thus far, with a jampacked mix of central bank decisions, critical economic data, and major corporate earnings announcements. Friday’s deadline for tariffs taking effect also looms large. In the U.S., although the Fed is widely expected to leave interest rates unchanged on Wednesday, attention will be focused on any forward guidance as conflicts with the administration escalate. Fed funds futures currently imply around a 65% probability of a rate cut in September, a number that could swing significantly depending on the tone of Powell’s statement. The first estimate of Q2 GDP also arrives on Wednesday with projections for 2.5% growth. The monthly employment updates are sprinkled throughout the week, culminating in Friday’s non-farm payrolls. The core PCE price index, ISM manufacturing PMI, and revised consumer sentiment figures are the other main releases to watch. Earnings reports from mega caps like Apple, Amazon, Meta Platforms, and Microsoft have market-moving potential, given their outsized influence on U.S. equity indices. On the international side, the Bank of Japan is expected to keep rates steady as political pressure may mount following last week’s election results. Rates are also expected to stay on hold in Canada as the country continues to seek a trade deal with the U.S. Finally, inflation updates from Australia and the Eurozone, along with China’s PMI releases, round out the overseas agenda.

CHART OF THE WEEK

Weak dollar ripple effects

The downward pressure on the U.S. dollar has been relentless in 2025, which has had varied effects on other asset classes. A currency’s value is typically measured in terms of another, and given the dollar’s dominance in global trade, it is usually compared against a basket of other currencies, which can be weighted in different ways. One method is to use the nominal broad U.S. dollar index—what used to be known as the trade-weighted U.S. dollar index. It provides a weighted average of the dollar against a broad group of major U.S. trading partners. This year, the index has slumped just over 7% from the highs in early January. A weaker dollar typically boosts the overseas earnings of U.S. companies by making their exports more attractive in those markets. During the current earnings season, several large multinational corporations have reported higher profits and an improved annual forecast due to the weaker dollar. Nearly 40% of revenue from S&P500 companies comes from non-U.S. markets, so the currency factor could be a considerable tailwind if the dollar continues to decline. However, it remains to be seen whether this lift is sustainable. Investors may cheer the currency-driven gains in the short term, but organic growth in revenue and earnings tends to be the most important factor for equity returns over the long run. Furthermore, the dollar could stabilize once the world adjusts to shifting trade policies. In the meantime, two sectors that typically have the most international exposure are technology and industrials, which are the best performers this year. Consumer discretionary and healthcare also have significant overseas sales, but these sectors are down slightly in 2025.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.