Weekly Newsletter July 28th to August 1st

RECAPPING LAST WEEK

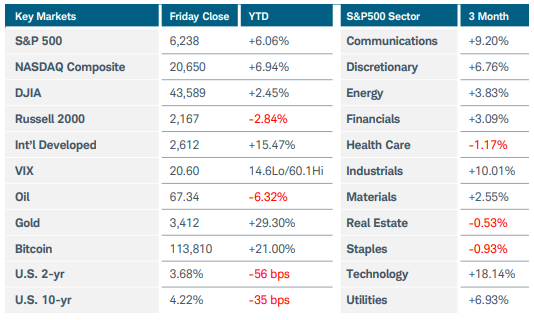

Investors flipped to a risk-off mode late last week after a weak jobs report and the White House’s new tariff rates announcement sent global equity indices sharply lower. The S&P500 and Nasdaq Composite indices fell more than 2%, while the Russell 2000 tumbled 4%. Ten of eleven S&P500 sectors lost ground, with utilities being the lone gainer. Technology fell 2% despite strong earnings reports from Microsoft, Meta Platforms, Amazon, and Apple. Friday’s shocking non-farm payrolls report caused the U.S. dollar to give back more than half the gains it made during a rally earlier in the week; the report also sent Treasury yields nosediving. July payrolls increased by just 73,000— this, combined with large downward revisions to prior months, left three-month average growth at an anemic 35,000. The unemployment rate held steady at 4.2%, largely due to a substantial drop in workforce size. Earlier in the week, the Federal Reserve decided to keep interest rates steady, a decision that may come back to haunt the central bank. Two FOMC members voted against the decision—the first such dissent since 1993—citing rising threats to the labor market. The June PCE price index revealed an uptick in headline inflation, rising 0.3% MoM and 2.6% YoY, while the core rate held steady at 2.8% YoY. Although tariff effects have yet to manifest significantly in consumer price data, the latest wave of import duties may put the Fed’s 2% inflation target further out of reach. In other economic news, U.S. GDP rebounded more than expected in the second quarter, increasing at a 3.0% annualized rate. The reading continued to be heavily distorted by trade, however, as the record import deficit from Q1 reversed course. Underlying measures such as final sales to private domestic purchasers suggested slowing demand. The ISM manufacturing PMI dropped to 48.0 in June from 49.0 while the employment index plunged to the lowest level since June 2020. Overseas, the Bank of Japan kept interest rates unchanged while raising its inflation forecast and offering a less gloomy economic outlook, suggesting that rate hikes could resume later this year. The Bank of Canada also kept rates steady mid-week, citing the uncertainty around U.S. trade policy that flared up again on Friday. In Europe, economic growth was better than expected in Q2 but still tepid at +0.1% while July’s inflation reading held steady at 2%. Finally, China’s manufacturing PMIs pointed to a stronger contraction last month.

THE WEEK AHEAD

Investors will see a break in the onslaught of economic data this week, but last week’s late selloff and the ongoing uncertainty around trade deals have the potential to keep volatility elevated. While Fed dissenters Waller and Bowman felt the committee was being overly cautious and that tariffs were thus far only having limited impact on prices, financial markets may just be waking up to the potential implications from significantly higher pre-trade war tariff levels. In last week’s press conference, Chair Powell went so far as to say one could argue the Fed is looking through goods inflation by not raising rates. Labor market concerns seem to be the main reason investors are still pricing in two rate cuts by year-end. In the U.S., 10- and 30-year Treasury auctions along with ISM services PMI are the main economic releases, while factory orders, preliminary Q2 productivity and unit labor costs, and consumer credit figures round out the domestic agenda. With the Fed’s quiet period over, look for appearances from committee members sprinkled throughout the week. The busy part of earnings season has passed, but reports this week from Palantir, Advanced Micro Devices, Caterpillar, Uber, Disney, and McDonalds will likely garner attention. On the international side, the Bank of England is expected to cut rates by 25 basis points in a close vote, despite concerns about the recent inflation uptick. China’s trade and inflation data and the Bank of Japan’s Summary of Opinions are the other releases of note.

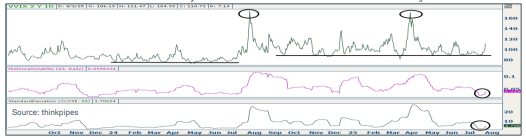

CHART OF THE WEEK

Volatility compression

Many catalysts for market downturns can appear unexpectedly—hence, the difficulty in predicting them. The Japanese yen’s sudden spike that roiled markets one year ago is a recent example. August and September have historically been among the weakest months for equity indices, and Friday’s drop may portend a similar outcome for 2025. The S&P500’s relentless advance since April’s initial tariff scare looked to be overextended when analyzing technical and sentiment indicators. Before Friday, SPX had not closed below its 20-day simple moving average (SMA) since April 23, the longest streak in more than 50 years. The index’s 20-day historical volatility had also fallen to around 6.5%, the lowest level since mid-December. The VIX fell to its second lowest level of the year early last week before jumping above 21.50. Another interesting sentiment indicator is the VIX Volatility index (VVIX), which measures the expected volatility of the 30-day forward price of the VIX—in essence the volatility of volatility. Looking at the chart below, a few things stand out. First, a higher floor around $90 has been established since the events of last August, with those highs nearly being repeated in April. Second, both the 20-day historical volatility and standard deviation studies plunged to levels not seen since last summer, just before the yen debacle. Investor complacency does not mean that a market correction is imminent, nor does it forecast the magnitude of a pullback. However, if unexpected shocks arise, such as last week’s disappointing jobs report, this complacency may prove fragile and lead to volatility spikes. While prolonged stretches above the 20-day SMA tend to be positive for forward equity returns, chances for the first downturn of any substance in more than three months may be on the rise.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.