Weekly Newsletter July 6th to July 10th

RECAPPING LAST WEEK

Concerns over the durability of the artificial intelligence rally and renewed geopolitical tensions in the Middle East dominated global equity markets this week. Selloffs in memory chip companies early in the week were tied to Samsung’s preliminary earnings report, in spite of the fact that the company forecasted a nearly 20-fold year-over-year increase in profits. Shares sold off 10% over worries that hyperscalers’ demand could fall. Late in the week, SK Hynix—another South Korean memory chip maker—countered this narrative, raising $26.5B in a 7x oversubscribed offering that marked the largest ever offering of shares by a foreign company in the U.S. This provided support to the thesis that investors still have an appetite to fund the enormous capital needs of the AI infrastructure buildout. Renewed hostilities in the Middle East prompted by the IRGC firing upon three ships transiting the Strait of Hormuz led President Trump to declare the cease fire over. The next two nights saw intense attacks against Iranian coastal installations intended to degrade their ability to further disrupt shipping. Before these events, crude oil prices had eased all the way back to pre-war levels. They spiked on the news but eased somewhat after Trump claimed that Iran was still interested in making a deal. Understandably, this all led to a great degree of sector churn as defensive names and energy benefited early in the week before risk appetites resumed later. S&P 500 sector wise, Energy, Technology, and Communication Services were the strongest performers, while Materials, Healthcare, and Consumer Staples were the weakest. The rise in energy prices and release of the FOMC minutes, which expressed concern that a combination of energy prices and massive AI buildout expenditures could keep inflation elevated, affected Treasuries as well. Yields on the long end of the curve pushed through 4.5% on the 10 year and back above 5% for the 30 year. In other macro sectors, precious metals were flat, the dollar eased slightly and the late week resumption of risk appetites firmed crypto a bit.

THE WEEK AHEAD

Markets will turn their attention to the 2nd quarter earnings season kickoff, with reports from the major money center and investment banks. Investors will focus not only on the fundamental line items like interest margins and loan growth, but also on commentary concerning the health of the consumer amidst the broader economic backdrop. Midweek sees earnings announcements from AI/Tech supply chain bellwethers Taiwan Semiconductor and ASML, as well as Netflix’s announcement, which offers insights at the intersection of tech and consumer discretionary. The release of CPI on Tuesday will offer fresh inflation data, but the big news is expected to come from Fed Chair Warsh’s first semi-annual Humphrey-Hawkins testimony to the House Banking Committee, where he’ll deliver the Fed’s Monetary Policy Report and field questions. Wednesday offers additional inflation data with the release of PPI. The other notable events on the economic calendar are retail sales and pending home sales data on Thursday, with more housing data coming on Friday with the new home sales reading. The renewed uncertainty in the Mideast will surely keep energy markets on edge and could catalyze either risk-on moves into tech or a risk off move to defensive sectors like healthcare and consumer staples.

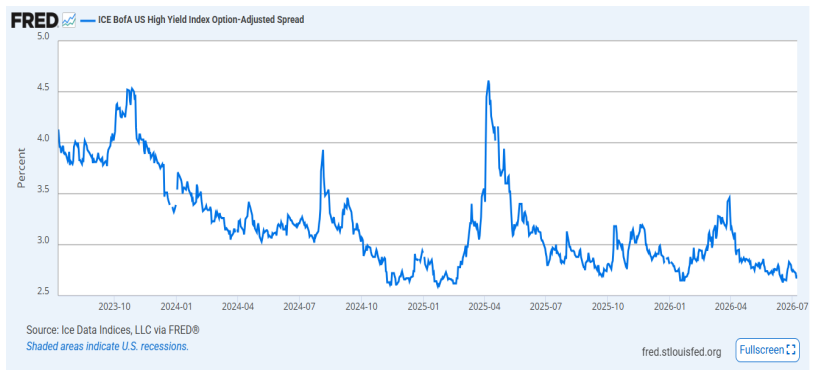

CHART OF THE WEEK

Credit Where Credit’s Due

Market headlines only tell us part of the story about our financial situation. It’s an important part, of course, but headlines tend to focus on big, eye-catching headlines that can attract readers. Think Fed policy updates, Iran war news, and AI capex spending records—they’re exciting to read and stoke fear in investors’ minds. And certainly, they could influence markets and lead to a downturn in equities yet haven’t to any meaningful degree. Credit spreads, on the other hand, are not very exciting, and at least recently haven’t stoked investor fears. Still, credit spreads reflect not just what could happen, but what’s happening now. And what’s happening now is that these spreads are scraping record lows. The ICE BofA US High Yield Index Option-Adjusted Spread below shows the difference between high yield bonds vs Treasuries over the last 3 years. After a rough 2022 the spread gradually narrowed to current levels over a period of years. But recently, only brief periods of concern over tariffs and the war have had an impact. When lenders start to worry about repayment, lower grade bonds start requiring higher rates to warrant the risk. These low levels indicate lenders have very little concern in corporations ability to satisfy their obligations, despite the large size of the loans. Volatility can ebb and flow in equities but as long as credit spreads stay small, further expansion is likely to push through the fear in the headlines.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.