Weekly Newsletter July 7th to July 11th

RECAPPING LAST WEEK

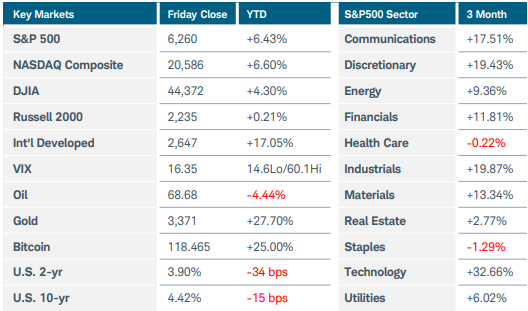

U.S. equity indices wobbled but still stayed near all-time highs despite additional trade war and tariff escalations. The S&P500, Nasdaq Composite, and Russell 2000 indices all finished marginally lower for the week. Six of eleven S&P500 sectors lost ground, including technology which failed to close higher even as Nvidia became the first company to exceed a $4 trillion market capitalization. In the commodity space, copper futures soared nearly 9% after President Trump proposed a 50% tariff on imports of the metal, which is a critical component of military hardware, electric vehicles, and many consumer goods. Gold futures rose more than 1% while silver prices spiked 5.5% to $39.15—their highest level since September 2011. Crude oil gained 2% after OPEC ministers and heads of western oil majors said that recent output boosts are not leading to higher inventories, which suggests an increase in global demand. Bitcoin jumped 7% to fresh record highs above $118,000. Auctions for 10- and 30-year Treasuries were met with solid demand but yields still pushed higher by week’s end. Aggressive tariff talk directed toward Japan, South Korea, Brazil, and Canada heightened inflationary concerns. The U.S. dollar also rose as currency traders speculated that tariffs may not damage the U.S. economy as much as initially feared and that interest rates could remain at or near current levels. Turning to economic data, Americans’ inflation outlook was little changed last month while households grew more optimistic on their finances, according to the New York Fed Survey of Consumer Expectations. Small business confidence slipped slightly in June as firms fretted over excess inventories. Minutes from the most recent FOMC meeting revealed that expectations for how tariffs might impact inflation differed. New rate projections showed that 10 of 19 officials expect at least two rate cuts by year end, seven members project no cuts, and two members expect only one. Overseas, Australia’s central bank chose to wait for more confirmation that inflation was easing before cutting rates, surprising market participants. Governor Bullock said the bank remained committed to loosening monetary policy provided that Q2 CPI is in-line with forecasts. China’s producer price index continued to tumble, falling 3.6% YoY in June. Consumer inflation edged slightly higher but domestic demand was still weak, adding pressure on policymakers to provide additional fiscal support. In Europe, the investor confidence index rose 4.4 points this month to reach its highest level since February 2022. Finally, Britain’s economy contracted for a second straight month in May, dashing hopes for Q2 GDP growth and adding to rate cut expectations.

THE WEEK AHEAD

Investors continue to shrug off the trade war drama, with the Cboe Volatility index falling to a five-month low of 15.70 last week. However, the recent rally in stocks will be tested this week by a slew of economic data, highlighted by U.S. inflation figures, retail sales, and corporate earnings announcements. The forecast for Tuesday’s June U.S. CPI release is a 0.3% increase, up from the prior reading of 0.1%. Economists expect this report to be the first where inflationary effects from tariffs could show up, and any upside surprises could rankle markets. The producer price index will follow on Wednesday. The resilience of U.S. consumers has been impressive, and Thursday’s retail sales report is expected to show a rebound from the prior month’s drop. The large U.S. banks—most of which recently raised their dividends and announced new share repurchases after passing the Fed’s annual stress tests—will kick off earnings season this week. Netflix, Taiwan Semiconductor, PepsiCo, and 3M are among other companies of note scheduled to report. The rest of the domestic calendar features Empire State and Philly Fed manufacturing indices, building permits and housing starts, and this month’s preliminary consumer sentiment reading. On the international side, later tonight China will release GDP, industrial production, and retail sales data for June. The UK reports crucial inflation and employment figures, while economic sentiment surveys are on the docket for Germany and the wider Eurozone. Japan’s nationwide CPI rounds out the week ahead.

CHART OF THE WEEK

Evolution of a crypto trend

Bitcoin first reached $110,000 in January before trending lower through Liberation Day in early April to below $75,000. From a technical perspective, those lows coincided with a significant MACD bullish divergence, followed by a break above down-sloping resistance and the 50-day exponential moving average. The ensuing uptrend was quite orderly—particularly for a volatile asset such as Bitcoin—as price rallied almost exactly 50% over the next month to $112,000. Sideways consolidation then set in until last week when price again broke through resistance, liquidating over a $1 billion in short positions in a single day on its way past $118,000. There are several fundamental factors fueling this rally. One is rotating supply, with many long-term Bitcoin holders taking profits and institutions stepping in to absorb those sales. Bitcoin fund inflows have been strong with $1.18 billion last Thursday alone, bringing the year-to-date total to more than $50 billion. Another factor is the upcoming “Crypto week” in Washington, with three bipartisan bills up for debate in the House of Representatives that could provide a long-needed clearer regulatory framework for the industry. Cryptocurrencies will likely remain among the most volatile asset classes, but technical and fundamental tailwinds are propelling Bitcoin to new heights.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.