Weekly Newsletter June 15th to June 19th

RECAPPING LAST WEEK

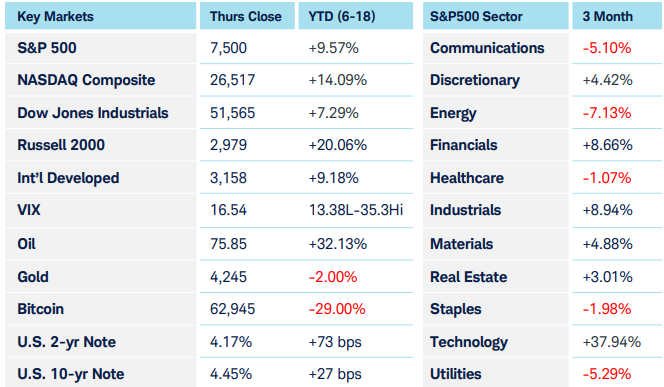

As the week began, investors extended the previous week’s relief rally, fueled by news of a deal to end the U.S. Iranian conflict and the potential that the Strait of Hormuz may reopen soon. Lower energy prices supported the Industrials and Materials sectors, and Technology benefited from the overall improvement in risk sentiment. The Energy sector and Healthcare were the biggest losers. The Federal Reserve’s June meeting, the first chaired by Kevin Warsh, stole focus by midweek. Policy makers left the Federal Funds target rate unchanged at 3.5%-3.75%, surprising no one. The only surprise investors hadn’t anticipated was the hawkish tone of the accompanying projections and commentary delivered in the press conference. Near-term rates rose in the wake of the announcement, flattening the yield curve. Investors on the long end took comfort, hoping the Fed was positioning itself well should inflation accelerate in the future. Despite borrowing costs, economic data painted a picture of a resilient economy, buoyed by higher-than-expected retail sales, and expectations that prices at the pump will decline sharply, providing additional consumer relief. The prospect for higher U.S. short term rates and an easing of the pressure on foreign central banks to hike rates led the dollar to rally to one-year highs. Precious metals finished the week marginally lower, as the countervailing forces of a strong dollar overcame their recent tendency to behave more like a risk asset than a defensive safe-haven. Crypto seems to be fading into the background, under pressure from a surging dollar and “risk-on” traders who are focusing on the semiconductor and AI space.

THE WEEK AHEAD

This week is likely to be dominated by the ongoing tug-of-war between resilient economic growth and central banks’ inflation containment efforts, though the sharp decline in energy prices certainly makes the banks’ situation easier. PMI data from Australia, France, Germany, the U.K. and U.S. will release on Tuesday. Last month’s data from this group highlighted a divergence: the Manufacturing component (excluding France) expanded while the Services component (excluding U.S.) contracted. It’s generally accepted that the services sector responds to challenging economic conditions more quickly than the manufacturing sector. The prices paid component will offer a view into inflation seen via business input prices. CPI data will be released for Canada on Monday and Australia on Wednesday, followed by PCE, “the Fed’s preferred inflation gauge” on Thursday.

CHART OF THE WEEK

Energy’s Squeeze

Among the eleven broad S&P sectors, energy has been the strongest performer year-to-date, though last week’s price action was notably weaker. The XLE chart represents an ETF comprised of companies in two groups: the oil, gas, and consumable fuels, combined with the energy equipment & services. The entire Energy sector constitutes 3.5% of the S&P 500 as of May 29, 2026. Bollinger bands, based upon the standard deviation concept, help visualize how prices are dispersed around an average value. At a traditional default setting of a 20-period moving average value (the middle turquoise line), the bands are established at 2 standard deviations above and below (each purple line) to encapsulate 95% of the price action over the past 20 periods. In a bullish environment like the one we saw from January through late March, prices can meet the upper Bollinger band in a recognizable uptrend as the band itself expands upwards. A strong uptrend occurs when prices find support at an upsloping 20-day moving average, as occurred several times during this period. Since early April, XLE has been in a range of welldefined price consolidation, with the lower levels showing support near the lower Bollinger band. The bands expand and contract over time, reflecting higher or lower degrees of statistical price volatility. More recently the bands have “squeezed” a bit, while price has consolidated. An interpretation chart followers can make is that a more sizable bout of volatility might follow these consolidations, or “squeezes”. With XLE priced near a key $54 support value, a bounce upward at support or a breakout down and through this key level could signify either a resumption of the prior uptrend or a reversal into a downtrend.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.