Weekly Newsletter June 22nd to June 26th

RECAPPING LAST WEEK

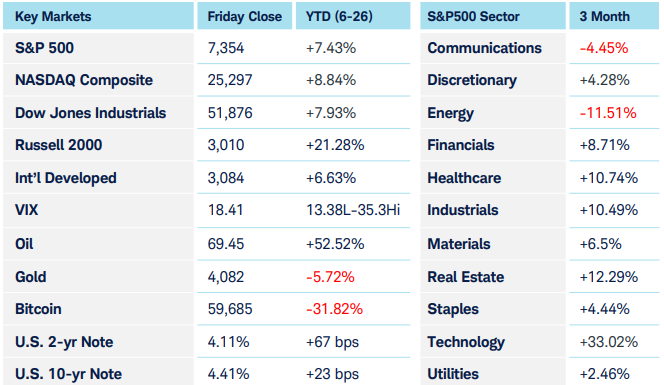

Last week’s overarching story in equity markets was the artificial intelligence trade—after an extraordinary run, investors decided it had become overextended. Heavy declines in Samsung Electronics and SK Hynix fueled an over 10% decline in South Korea’s KOSPI index on Tuesday, a market that is still up 125% YTD. At midweek, all eyes turned to Micron Technologies quarterly earnings—where the company delivered another exceptionally strong report that reinforced expectations of ongoing robust demand for memory chips. However this story, which reinforced the bullish case for AI-related capital spending, was undercut by Apple’s subsequent announcement that they would no longer absorb surging chip costs, and therefore raised prices on their laptops, tablets, and other devices. This led to a selloff in several of the companies’ “Magnificent Seven” peers. Defensive names were the biggest beneficiaries of the rotation: Healthcare, Utilities, and Consumer Staples sectors gained, while Consumer Discretionary and Communication Services were pressured along with the Technology sector. Despite the churn in equities, the broader macroeconomic backdrop remained relatively constructive—crude oil’s decline to pre-war prices below $70 per barrel helped temper inflation concerns, leading to modest declines across the Treasury yield curve. Declines in energy prices and inflation expectations impacted precious metals, as did strength in the dollar, which is just off its 1-year highs. In an interview on CNBC, Secretary Bessent used Venezuela’s and Iran’s new ability to sell oil for dollars to outline a vision that would not only maintain but expand the dollar’s central role in international trade and as the world’s reserve currency. Bitcoin meandered near its one-year lows, as investors found no support for crypto assets in any of this news.

THE WEEK AHEAD

The U.S. Employment report will certainly be the highlight of this shortened holiday week that ends the first half of 2026. From March through May the economy generated an average of 155k jobs per month. Economists, who vastly underestimated each of those figures now expect that the U.S. will have created 114k jobs in June. Other labor market data will serve as appetizers to Thursday’s main course, including the JOLTS jobs openings report on Tuesday and the ADP private payrolls report on Wednesday. Stronger-than-expected figures from these reports could increase the odds of a 25 bps hike in the Federal funds rate as soon as late July’s FOMC meeting—those odds currently sit at just 30%. While crude oil’s sharp decline has certainly helped temper longterm inflation expectations, those declines have yet to filter down to consumers at the pump. “Crack spreads”-a proxy for refining margins, remain near their wartime highs. Economists refer to this well-understood phenomenon as “Sticky downward prices”—it occurs when the decline in price of a finished good (gasoline) lags a decline in the price of its input (crude oil). The Russell indices will rebalance on Monday, driving additional intramarket activity following on from the divergence in memory chip suppliers and buyers last week. The most notable event will, of course, be the addition of SpaceX to the large cap Russell 1000 index along with pre-positioning flows ahead of its anticipated addition to the Nasdaq 100 Index on July 6th .

CHART OF THE WEEK

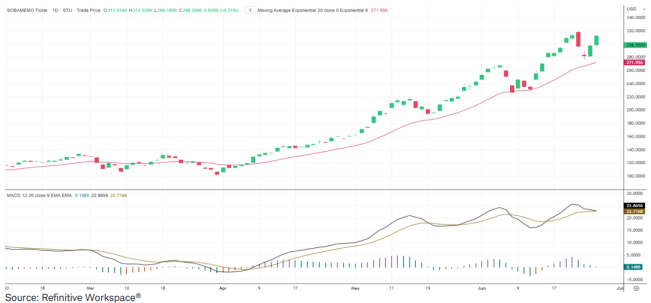

Memory’s regime change

The chart below shows the Solactive memory index, which helps highlight the most recent bottleneck in the AI stack. The primary driver within this index also mentioned above is MU, whose earnings last week changed the outlook for not only the memory and broader AI sectors, but inflation expectations as well. The company’s results were staggeringly high, but the bigger story was management’s announcement that, thanks to long-term supply agreements, the company’s entire production of high bandwidth memory (HBM) is sold out for years to come. Demand for memory has historically been cyclical, which means these stocks typically offer a lower multiple on earnings than a sector that experiences consistent demand year over year. AI seems to be changing this expectation, trading cyclicality for consistency in the industry. This not only means blowout earnings for all the memory companies but also should eventually result in an adjustment to their stock prices from a rising multiple. The memory index has tripled since April and is showing no signs of weakness yet, finding support at the 20-day EMA (the red line) and confirmation from the MACD study below. This implies that AI companies can anticipate vastly increasing hardware costs at a time when they have already begun passing these costs on to consumers, which only adds to the already sticky inflation situation. As long as the memory space displays consistent dominance the AI investment cycle remains intact.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.