Weekly Newsletter June 8th to June 12th

RECAPPING LAST WEEK

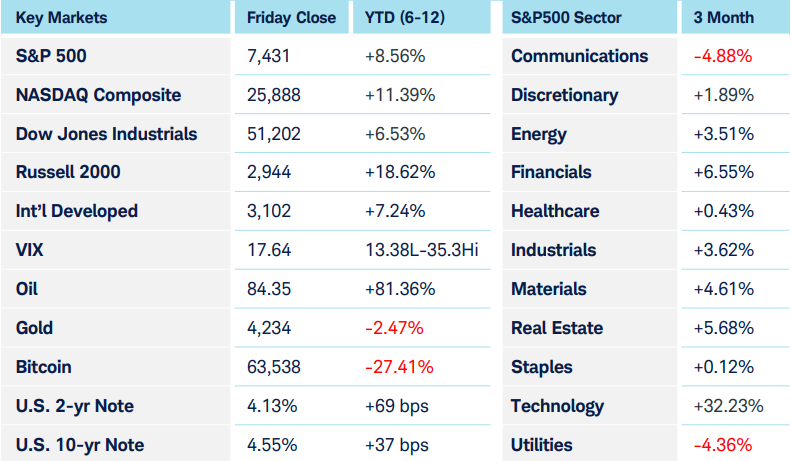

The week before last ended with a sharp selloff in the wake of a stronger-than-expected U.S. employment report, leading the dollar and Treasury yields to surge. Last week started with investors attempting to recover—major benchmarks regained their footing as the same semiconductor and artificial intelligence-related shares that bore the brunt of the previous week’s correction stabilized. As the week progressed, investors focused primarily on inflation data and central bank developments: The ECB raised rates from 2% to 2.25% in an effort to counter energy-driven inflationary pressures. In spite of this tightening, negative real interest rates are still providing a stimulative environment. Risk appetites mostly improved in equity markets thanks to welcome signs that price pressures were not rising as quickly as some had feared. Almost all S&P 500 sectors were in the green, with Materials, Consumer Staples, and Technology leading the way while Communication and Energy were the laggards, finishing a touch under unchanged. Developments in Iran drove commodity markets. On the one hand, tensions flared after the downing of a U.S. Apache helicopter and resulting U.S. retaliation against Iranian military sites near the Strait of Hormuz. On the other, hints of a potential agreement between the countries eased pricing pressure somewhat. Crude oil shrugged off the flareup, with prices reflecting acceptance of Trump’s claim that the U.S. had escorted tankers containing 100 million barrels of oil through the Strait. Precious metals declined sharply until midday Thursday, when Trump announced that he had called off a planned attack and seizure of Iranian oil infrastructure on Karg island—at that point they rallied along with other risk assets. Crypto responded accordingly with a knee-jerk rally joining the risk on group, but otherwise was quiet as Bitcoin spent the week consolidating near its YTD low-50% off October’s all-time high. Friday saw the public market debut of SpaceX, whose IPO valued the company at $1.77 trillion but quickly rose above $2 trillion when trading opened on the secondary market.

THE WEEK AHEAD

The week’s global economic calendar will focus on the central banks’ response to new inflation-related data. The Bank of Japan is widely expected to hike rates at the conclusion of its two-day meeting on Tuesday. As with the ECB, the expected tightening—in the BOJ’s case to 1%, still leaves the bank firmly in a stimulative posture, with negative real rates. The Reserve Bank of Australia, which was ahead of its central bank peers in hiking rates to counteract inflationary pressures, is expected to pause at their current 4.35% overnight cash rate when they issue their policy statement on Tuesday. In the UK, CPI is released on Wednesday, followed Thursday by the Bank of England, which is expected to hold rates steady at 3.75%. Back in the U.S., retail sales are released on Wednesday, but more importantly it’s also the day when new Fed Chair Kevin Warsh oversees his first meeting of the FOMC. Although the market is not expecting any move in rates, the press conference will act as his public debut and give observers their first meaningful opportunity to gain insights into his outlook. The current assumption is that Warsh views the path to being able to eventually lower interest rates as being a reduced balance sheet in combination with outsized gains in productivity fueled by AI, even as the market deals with inflation that for now is stubbornly above the Fed’s target. U.S. equity markets went into this past weekend with cautious optimism that a Memorandum of Understanding agreement could be finalized between the U.S. and Iran. While a number of potential agreements have been floated in recent weeks, this was the first to suggest a formal signing ceremony with V.P. Vance representing the U.S. However, midday Friday the Iranians leaked details framing the agreement entirely as a list of U.S. concessions, drawing the ire of the U.S, which fueled uncertainty about whether an agreement would be finalized over the weekend after all.

CHART OF THE WEEK

One of these metals is lying, but which one?

When it comes to metals markets, gold and silver get all the attention, but copper deserves a seat at the table. All three metals have for many years been positively correlated, with increases driven primarily by higher inflation and liquidity conditions. Over recent decades, the fact that oil-based transactions were denominated in dollars meant the U.S. currency was the standard store of value for central banks around the world. In recent years, some have questioned the dollar’s primacy, partially due to the accelerating national debt, but even more so after the U.S. seized over $300 billion in Russian-owned treasuries in May of 2023. This signaled to the world that treasuries weren’t safe and led some to balance their treasury holdings with gold and silver. The total value of all gold and silver assets above ground is 30% smaller than the treasury market, and much of that is not readily available. Add in elevated inflation and the result has been a 3x (gold) and 5x (silver) rally over the past three years, pulling both metals deep into overbought conditions. Meanwhile, AI data center construction and electrical grid enhancements increased to record levels, boosting demand for copper just as gold and silver hit exhaustion. The historical influences that caused the three metals’ prices to correlate were still at play but overpowered by the altered macro climate. Below, the US Copper Index (CPER) is displayed in candles, with the Gold and Silver index (XAU) in purple. The lower subgraph is the relative strength between the two. The reversal higher in relative strength marks the point when copper took the lead that it has held ever since. Copper prices have ONLY doubled since that low in 2023, but the gold and silver reversal earlier this year did not faze copper, which is 5% below its all-time high set in May and marching higher with no immediate signs of slowing down.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.