Weekly Newsletter March 2nd to March 6th

RECAPPING LAST WEEK

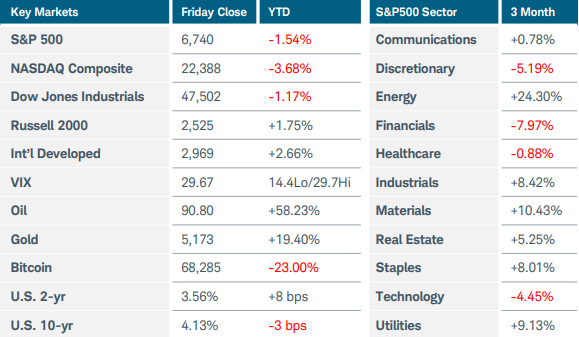

The conflict raging across the Middle East spiked oil prices to the highest level in more than two years, pressuring risk assets across the globe. U.S. equity indices held up better than their international counterparts, with the Nasdaq Composite down just over 1% while the S&P500 fell 2%. The MSCI EAFE and Emerging Market indices both tumbled close to 7% as disruptions to energy supplies threatened to derail economic growth in Europe and Asia. A sharp rally in the U.S. dollar also weighed on international stocks and most commodities outside of oil. Gold fell 2.3% while silver plunged 10%. Crude oil futures soared to $92.61 before settling around $91, up 35% for the week. Fears of rising inflation spurred by higher energy prices led to a jump in U.S. Treasury yields. Friday’s shocking non-farm payrolls report only briefly slowed the ascent: the U.S. economy unexpectedly shed 92,000 jobs in February and the unemployment rate ticked up to 4.4%. While a strike by healthcare workers and severe winter weather were cited as contributing factors, there was enough weakness across the report to raise concerns about broader labor market deterioration. In other economic news, January’s delayed retail sales figures revealed a 0.2% decline MoM, coming in below the expected flat reading. However, other data suggested that economic growth may yet accelerate in the first quarter of this year. U.S. business activity continued to expand last month, with the ISM manufacturing PMI registering 52.4 while services jumped to 56.1, its highest reading since July 2022. Survey respondents remained wary of tariffs, as the manufacturing prices paid subindex soared to 70.5 from 59.0. On Wednesday, Treasury Secretary Bessent said a 15% global tariff—rising from its current 10% rate—will likely be implemented soon under Section 122 of the Trade Act of 1974. Overseas, Eurozone inflation rose last month and may rise further if war in the Middle East leads to sustained higher energy prices. CPI increased to 1.9% YoY from 1.7% while the core measure jumped to 2.4% from 2.2%. Producer prices also rose in January, ahead of the consumer data. UK government bond yields surged as a doubling in gas prices cast doubt on the central bank’s ability to cut rates this year. In a budget update speech, finance minister Reeves acknowledged the risks facing Britain, which has the highest inflation among developed economies and is heavily exposed to energy cost impacts from the assault on Iran. Australia’s economic growth gained momentum in Q4 2025, reigniting price pressures and keeping further rate hikes on the table. Finally, China’s official PMIs stayed in contraction territory last month as domestic demand remained weak.

THE WEEK AHEAD

The sudden outbreak of war in the Middle East has changed everything. Artificial intelligence, private credit, and other concerns took a back seat as investors were consumed by skyrocketing energy prices and a sharp rise in both volatility and interest rates. President Trump’s demand for Iran’s “unconditional surrender” suggested that a swift end to hostilities may prove difficult. Qatar’s energy minister said that producers may need to invoke force majeure, which could shut down production and send oil and gas prices even higher. The conflict also puts the Federal Reserve in a tough spot, attempting to balance the impact of last week’s surprise decline in payrolls—which could lead to a drop in economic growth—against the potential that inflation could spike. While traders still think the Fed will not adjust rates at the March or April meetings, odds for a cut at the June gathering crept back above 50% after the weak jobs report. This week’s U.S. economic data is focused on inflation, with February CPI arriving on Wednesday followed by the delayed January PCE price index on Friday. Both readings are expected to be steady compared to prior levels but still higher than the Fed would prefer and now vulnerable to increases in the coming months. There are 10- and 30-year Treasury auctions this week along with housing data, the second estimate of Q4 2025 GDP, and this month’s preliminary consumer sentiment reading. Oracle will report quarterly earnings after market close on Tuesday. The international calendar features China’s inflation update and monthly GDP figures from the UK.

CHART OF THE WEEK

Dollar catches a bid

The events of last week reinforced the United States’s role as a financial haven for liquidity and perceived stability. The U.S. dollar index ($DXY) jumped to the highest levels since late last year and hinted at a potential reversal of the downtrend that started in early 2025. The outbreak of war has triggered fears of energy supply shocks that could lead to a global economic slowdown. The strong outperformance of non-U.S. assets that has been in place for months took a hit last week, reflecting Europe’s and Asia’s sensitivity to energy disruptions in the Middle East. The U.S., as a net energy exporter, is less susceptible to these effects, but would not be able to increase production fast enough to replace volumes that travel through the Strait of Hormuz to Asian countries like Japan and South Korea. Meanwhile, Europe faces the challenge of refilling natural gas storage, and although the U.S. is the region’s second-largest supplier it cannot fully replace sources like Europe’s pipeline from Qatar. The rotation in equity markets was evident last week with the S&P500 down only 2% while the MSCI Asia-Pacific and EAFE indices suffered drawdowns of 6-7%. Japanese equites sank 5.5% while South Korea tumbled more than 16%. From a technical perspective, $DXY poked back above its 200-day exponential moving average and probed long-standing resistance levels. The energy supply risks, regional economic vulnerability, and renewed risk-off mentality seem to be pushing capital toward U.S. markets.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.