Weekly Newsletter March 30th to April 3rd

RECAPPING LAST WEEK

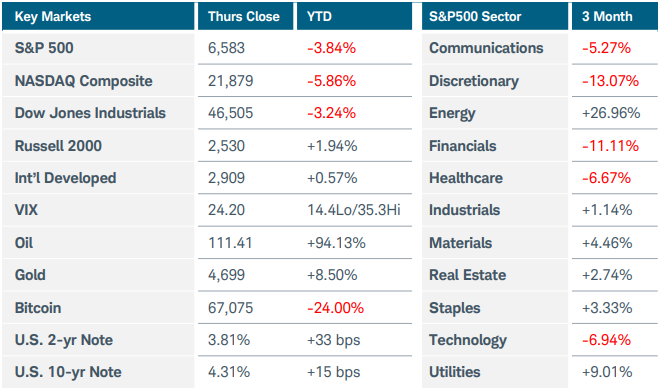

Despite the lack of a clear off ramp to the war in Iran, U.S. equity indices rallied sharply in volatile trading, posting their first weekly gain since the conflict began. The Nasdaq Composite index jumped nearly 4.5%, while the S&P500 and Russell 2000 each rose more than 3%. Crude oil futures surged by 11.5% on Thursday after President Trump vowed to strike Iran more aggressively, while Iran’s armed forces warned the U.S. and Israel of further retaliatory attacks in response. In contrast to stocks, which reversed from steep losses at Thursday’s open, oil was little moved by reports of Iran working with Oman to develop a collaborative framework to monitor traffic in the Strait of Hormuz. Ten of eleven U.S. sectors finished higher, with energy (-5.3%) the sole loser even as oil prices climbed. Gold and silver faded at week’s end, but each gained around 4%. U.S. Treasury yields eased as investors priced in the increasing likelihood of a global economic slowdown triggered by the war in the Middle East. Fed Chair Powell’s comments also contributed to the fall in yields—he said the central bank has little control over supply shocks that might be caused by the surge in oil prices, but that longer-term inflation expectations are not yet rising. Last week’s economic data suggested that the U.S. remains on solid footing—for now. March’s non-farm payrolls, released on Friday while U.S. equity markets were closed, rebounded more than expected with 178,000 jobs added. The unemployment rate fell to 4.3%. Other labor market data presented a mixed picture: private payrolls rose by 62,000, while job openings fell more than forecast and hiring dropped to the lowest level in six years. Layoffs at technology companies continued to increase, with artificial intelligence advancements cited as a main driver. The Commerce Department continued to catch up on data delayed by last year’s government shutdown, announcing that U.S. retail sales increased 0.6% in February. ISM manufacturing PMI lifted to 52.7 in March, the highest reading since August 2022. Part of the rise was due to increasing delivery times, which typically occur in a strong economy but in the current environment may indicate supply chain disruptions. The prices paid measurement jumped to 78.3 from 70.5. The Conference Board’s consumer confidence indicator, which generally focuses on labor market conditions rather than the cost of living, rose to 91.8 last month. Overseas, some 40 countries were engaged in virtual talks on Thursday, exploring ways to restore navigation in the Strait of Hormuz. Eurozone inflation spiked to 2.5% YoY in March, up from 1.9%. The rise was almost entirely due to rising energy prices. Manufacturers faced soaring input costs and supply chain disruptions, forcing them to raise prices. Germany’s top economic institutes cut their growth forecasts for this year and next and raised inflation projections. In Japan, core consumer prices in the country’s capital rose 1.7% YoY in March, a figure analysts expected to rise in the coming months. Japanese manufacturers expressed their highest level of optimism in more than four years, according to the Tankan survey. Finally, China’s official PMI surveys rose more than expected last month as production and new orders expanded.

THE WEEK AHEAD

Oil prices will remain the focus as investors struggle to process conflicting signals of when the Middle East conflict could wind down. OPEC+ was expected to consider additional oil output increases when it met on Sunday, but any action would have little impact on supply until the Strait of Hormuz is opened. In the U.S., Friday’s CPI report for March will be an important gauge of how the war’s energy shock is impacting the economy. While it may be too early to reflect any broader inflationary impact, the headline reading is expected to have jumped a whopping 1.0% MoM. Any upside surprises could further rattle fragile stock and bond markets. The PCE Core Price index will be released on Thursday, but that will be February’s delayed data. The rest of the domestic calendar includes ISM services PMI, minutes from the last FOMC meeting, 10- and 30-year Treasury auctions, and April’s preliminary consumer sentiment reading and inflation expectations. Developments in the private credit markets will likely remain in the headlines. Asset management companies were under pressure last week after Blue Owl limited redemptions in response to investors asking to withdraw 40.7% of shares in one private credit fund and 21.9% in another. The Treasury Department was expected to announce meetings with domestic and international insurance regulators to discuss transparency and lending practices in the industry. The international economic calendar features Eurozone PPI and retail sales figures, German industrial production and factory orders, and China’s monthly inflation update.

CHART OF THE WEEK

Sector woes

The S&P500 Financials sector ($SP500#40) dropped 15% from its January high before rebounding 3.5% last week and showing the first indications of a potential trend reversal. Financials were not the best performing sector but were the most notable positive sign considering its preceding downtrend. The index broke above its down-sloping technical resistance and the 20-day exponential moving average while a bullish divergence emerged in the MACD indicator. This accompanied a broad market rally on hopes of de-escalation in Iran and was aided by a drop in interest rates. Although financials represent just over 10% of the S&P500 index by market cap, their influence is greater than that figure would indicate, since strength in banks signals confidence in credit conditions and economic resilience. If the index can build on its initial signals and hold above last week’s low of $794, its progress could be contagious. Concerns about private credit woes spreading across the sector are a potential headwind, as are the war in Iran and the potential for a spike in rates that could flatten the yield curve further and hurt banks’ profits.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.