Weekly Newsletter March 9th to March 13th

RECAPPING LAST WEEK

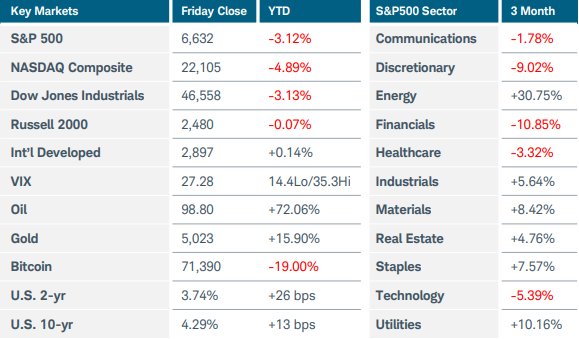

Escalations in the Middle East conflict raised fears regarding the largest potential oil supply disruption in history. During the week, crude oil soared to $119.50, then plunged below $77 before again ascending to nearly $99. It ended the week higher by 8% despite the International Energy Agency’s largest-ever release of 400 million barrels to try to reign in prices. The nauseating volatility left U.S. equity indices lower for the week; the S&P500 and Nasdaq Composite indices fell around 1.5% while the Russell 2000 dropped nearly 2%. Although the major indices avoided severe carnage, heightened volatility kept investors on edge. The VIX jumped above 35 before settling near 27, which still implied a 1.7% daily move for the S&P500. Nine of 11 sectors lost ground, with financials tumbling more than 3% on palpable private credit worries. JPMorgan Chase reportedly marked down some loan values held as collateral, reducing the ability of private credit firms to borrow against those loans. Gold and silver ended down 3% and 5%, respectively, while Bitcoin rose 4%, decoupling somewhat from the weakness in equities. U.S. Treasury yields surged as the risk of inflation from energy prices drove bond prices lower. Weak demand at auctions of 3- and 10-year notes also weighed on sentiment, along with investors digesting a record $66 billion in new corporate debt on Tuesday. In economic news, U.S. CPI rose 0.3% MoM in February, slightly above the prior reading. The delayed core PCE price index from January showed a 0.4% increase MoM and 3.1% YoY. Both reports suggested that prices were on the rise even before the outbreak of war this month. The second estimate of Q4 2025 GDP was revised lower to 0.7% growth from 1.4% on downgrades to exports and government spending. Final sales to private domestic purchasers, a closely-watched measure of domestic demand, slipped to a 1.9% gain from the initial estimate of 2.4%. Consumer sentiment slid to 55.5 this month from 56.6, with about half of the survey responses collected after the start of the U.S.-Israeli war with Iran. Inflation expectations for the next year were flat at 3.4%. Finally, housing starts and existing home sales rose to start the year as affordability improved and multifamily construction boomed. On the international side, major equity indices fell around 2%, pressured by a rising U.S. dollar and sensitivity to higher energy prices. In China, consumer inflation jumped by the most in three years while deflation in producer prices moderated. At an economic policy-setting meeting last week, the country lowered its GDP growth target to a range of 4.5% to 5%, its lowest goal since the early 1990s. China’s trade surplus rose to the highest level on record as exports surged 21.8% YoY in the January-February period.

THE WEEK AHEAD

In his first comments on Thursday, Iran’s new supreme leader Mojtaba Khamenei vowed to keep the Strait of Hormuz shut, leveraging the country’s strategic position in the Persian Gulf to hold the global economy hostage. Although an Indian oil tanker on Friday was among limited ships that have moved through the strait, and despite the IEA’s aforementioned release and the U.S. allowing countries to buy Russian oil from ships stranded at sea for the next 30 days, experts fear that only an end to the conflict would resolve the currently untenable situation. Any disruption in oil flows lasting more than a few more weeks would likely necessitate more inventory releases, and getting those barrels to market is a formidable challenge. In the midst of turmoil, investors will have six central bank decisions to mull over this week. In the U.S., the Federal Reserve is likely to hold rates steady as it faces prospects of higher inflation and a weaker labor market. The Fed will also update the Summary of Economic Projections midweek. Plenty of fresh uncertainty has been added to the outlook due to the Iran conflict. Fed funds futures aren’t indicating better than a 50% chance of a rate cut until the October meeting. The economic calendar features housing data, producer prices, and regional manufacturing surveys, while chip giant Micron Technology reports earnings on Wednesday after market close. Central banks in Australia, Canada, and Japan have rate decisions earlier in the week, followed by the UK and Europe on Thursday. While all are expected to leave rates unchanged, their statements will be scrutinized for any hawkish shifts in tone. Releases on the international economic calendar include China’s monthly data dump, German economic sentiment, Canadian CPI, and UK employment figures.

CHART OF THE WEEK

Shock at the pump

The surge in oil prices has consumers concerned about gasoline costs, which were already rising ahead of the war in the Middle East. Looking at the chart of the S&P GSCI Unleaded Gasoline index (SPGSHU), gas prices rose steadily from the beginning of the year, then gapped higher in early February when initial signs of trouble arose around the Strait of Hormuz. The oil price shock didn’t appear until nearly a week after the strait was effectively closed, but gas moved well ahead of that date. The gasoline index is now up 75% from pre-war levels. Prices at the pump tend to lag oil by one to three weeks, and the national average may move closer to $4 per gallon if oil remains near $100 or spikes higher. Governments around the world are scrambling for solutions, including reductions or temporary elimination of fuel taxes, in addition to oil stockpile releases. As long as the strait remains effectively closed, prices may continue their aggressive rise.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.