Weekly Newsletter May 11th to May 15th

RECAPPING LAST WEEK

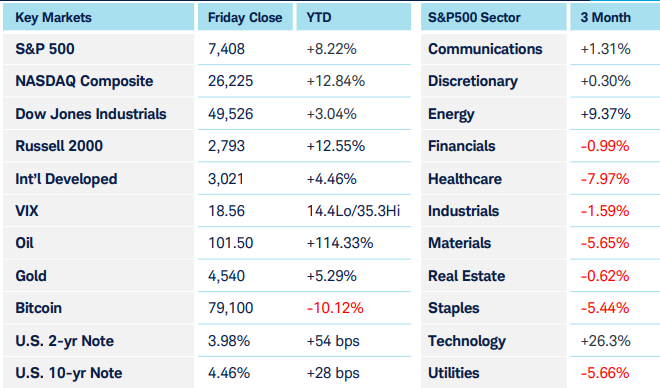

Major US equity indices pushed to fresh highs early in the week, as AI and semiconductor strength helped support the S&P500 and Nasdaq, before rising yields and renewed inflation concerns pressured growth stocks into the close. Market leadership remained narrow and tech-driven, with investors continuing to reward AIrelated earnings momentum, though high-multiple equities remain sensitive to any backup to rates. Treasuries weakened across all maturities flirting with some cases crossing psychologically important yield levels that also represent 1-year highs with 2 years at 4%, 10 at years 4.5% and 30 years poking through 5% for the first time since last summer. The catalyst was the hotter than expected CPI and PPI reports, showing year over year inflation running at 3.8% and 6% respectively which not only killed market expectations of any chance of a near term cut but meaningfully priced in chances for hikes by year end. Fed Funds Futures began the week at a 95% likelihood that the FOMC would hold rates steady at its June 17th meeting, with a 5% chance of a 25 basis point cut. Those figures ended the week at 99.2% and 0.8% respectively. Perhaps more importantly looking further out towards the last meeting of the year, the market now sets a 50% chance of no rate change, a 40% chance of a 25 bps hike and a 10% chance of a 50 bps hike. The dollar, while largely a nonevent for over a year, firmed a touch against all the major currencies through Thursday and moved sharply higher on Friday as part of the market’s realignment to pricing in a meaningful potential for rate hikes. Crude oil remained firm with the now active July contract hovering around $100 per barrel while the strong backwardation remains as the soon to expire June contract is trading north of $105. The cease-fire with Iran remained in place even as the U.S. dismissed that country’s conditions for reopening the Strait of Hormuz. This appeared to be driven more by the need to avoid distractions during the U.S./Chinese summit, rather than hopes for an imminent diplomatic solution. Precious metals were part of Friday’s overall “risk-off” trade despite holding firm earlier in the week, with silver down over 10% on the day. The U.S. delegation to the Beijing Summit included CEOs representing more than 20% of the market cap of the S&P 500, so the event had the potential to generate market moving news, though in reality few deals were announced. After the first day Reuters reported that Nvidia was granted approval to sell their 2nd tier H200 chips to 10 Chinese firms, but follow-up reporting implied that the Chinese were at best indifferent to this offer. The administration’s announcement that China had committed to purchasing 200 Boeing jets was the only other notable deal with numbers attached, and the President later commented to reporters that the final number could be as high as 750 if delivery of the first 200 goes well. Treasury’s Bessent also mentioned in an interview on Thursday that the US would be dropping tariffs against “cheap consumer goods” that the U.S. has no interest in manufacturing domestically but there wasn’t much in the way of follow up coverage. For the Chinese, attempting to alter the U.S’s “strategic ambiguity” policy concerning Taiwan was the main opportunity.

THE WEEK AHEAD

It’s said that the market likes to throw a challenge at new Fed chairs, and Mr. Warsh may certainly have one on his hands, given the political pressure to cut rates even as the markets have transitioned to pricing in hikes. Will skeptical FOMC members buy into his argument that large scale AI adoption will lead to a productivity boom that would offset any energy related inflation? Alternatively, he could argue simply that hiking rates isn’t appropriate to counteract a perceived short term supply shock in a key commodity that is already adversely impacting lower and middle income consumers. Global PMIs will be a key cross-market catalyst, with preliminary reading from the U.S., Germany, the Eurozone, and the U.K. helping investors assess whether global manufacturing and services momentum is improving or being pressured by higher input costs. Domestically, the U.S. economic calendar doesn’t offer much else in the way of impactful data this week. On the international front, Tuesday and Wednesday will offer a look at how the energy price spike is affecting Canadian and UK consumers with the release of their CPI reports and Australian unemployment figures are released on Thursday. With the Beijing summit in the rearview mirror, the focus will likely turn back to Iran. As of the time of this writing, diplomatic efforts seem stalled and the administration appears to be growing increasingly frustrated that efforts to get the Strait of Hormuz opened have yet to yield meaningful results. Speaking of yields, with rates across the curve sitting at, near, or just through one-year highs, some will wonder if Mr. Warsh will be dealing with “Bond Vigilantes” right out of the gate. The prospectus for the SpaceX IPO could be filed as early as this week, which would start the 20 day “quiet period” window before the IPO could occur. Some reporting has indicated that the roadshow will commence June 8th with a valuation of $1.25 Trillion, though the public offering will “only” be in the $70-$75 billion range. It’s yet to be determined whether SpaceX will be added to indices like the Nasdaq 100 imminently, a carrot that the exchange had been rumored to be offering as an incentive to secure the listing. At the $1.25T valuation, it would be the 10th largest component of the index, behind Meta (META) and ahead of Walmart (WMT), representing about a 3.5% weighting in the index. The QQQ ETF alone, with assets of $464B, would have to acquire about $16B worth of shares, over 20% of the public float. While we just addressed the largest anticipated IPO ever, it’s only fitting that we finish addressing the longest continuously listed security. On Thursday, the Bank of New York, founded in 1784 and first publicly traded in 1792 from the “Buttonwood Agreement” that laid the foundation for the NYSE, will change its ticker symbol from BK to BNY. Quite the legacy there, Mr. Hamilton.

CHART OF THE WEEK

The long end is getting high

The Fed views inflation above its 2% target as a threat to price stability, one half of its dual mandate. Inflation caused by increased confidence, it’s labeled a demand shock, potentially calling for tighter policies from the Fed to lower inflationary pressures generated by domestic demand. If it increases due to a rise in oil prices the economy is facing a supply shock, and raising interest rates could make a bad situation worse. This is precisely the predicament the incoming Fed chairman faces, and currently, the bond market appears to believe a rate hike is more likely. According to CME’s FedWatch, as of last week, there was a 98% chance the Fed will hold rates steady at June’s meeting while a 30% chance of hiking by December. The 30-year Treasury yield (chart below) highlights last week’s surge up and through the 5% level to a nearly 2-year high. The steady ascension with rising lows and a horizontal level of now-broken resistance is an ascending triangle price pattern, projecting higher rates to continue, aligning with incoming data.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.