Weekly Newsletter October 6th to October 10th

RECAPPING LAST WEEK

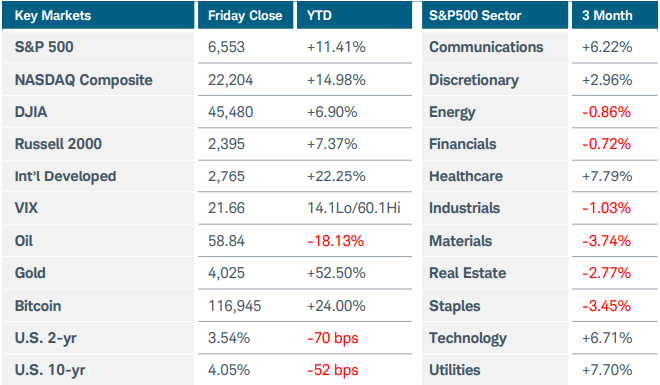

With the U.S. government shutdown ongoing and a dearth of economic data for investors to consider, U.S. equity indices drifted aimlessly until ending the week with a sharp selloff as trade tensions with China suddenly spiked. The major U.S. indices plunged 2.75% to 3.50% on Friday, finishing the week lower by similar percentages. Nine of eleven S&P500 sectors lost ground, with staples and utilities being the lone bright spots. Shares of technology stalwart Advanced Micro Devices surged 45%, ultimately settling 30% higher after the company announced a deal to supply artificial intelligence chips to OpenAI. Crude oil prices closed below $60 for the first time in five months—supply disruption fears dissipated after Israel and Hamas agreed to the first phase of a plan to end the two-year long war in Gaza. Gold prices leapt above $4,000 for the first time, buoyed by central bank buying and global economic uncertainty. U.S. Treasury yields rose early last week after 10- and 30-year auctions pointed to middling demand and comments from some FOMC members suggested caution in cutting interest rates. Minutes from last month’s FOMC meeting also revealed that the committee is still wary of inflation risks despite labor market weakness. However, by week’s end yields were lower as concerns grew over the economic impact of a prolonged government shutdown and new tariff threats. The limited data released during the week was mostly sentiment-based and indicated little optimism from Americans on improvements in the jobs market and inflation. October’s preliminary consumer sentiment index was little changed at 55—the lowest reading since May—while one-year inflation expectations remained elevated at 4.6%. Respondents to the New York Fed Survey of Consumer Expectations expressed heightened probability of both higher overall unemployment and odds of losing one’s job over the next year. Overseas, China tightened its rare earth export controls with plans to limit shipments to foreign defense and semiconductor manufacturers. The move prompted the Trump administration to threaten massive retaliatory tariffs, sending global risk assets tumbling to end the week. In Japan, hardline conservative Sanae Takaichi was set to become the country’s first female prime minister after winning the presidency of the ruling party. The result initially sent Japanese bond yields higher, and the yen lower, as the Bank of Japan may now get pushback on raising interest rates.

THE WEEK AHEAD

Volatility spiked sharply on Friday—the VIX index closed above 21—as skittish investors reacted to renewed tensions in U.S.-China trade negotiations. Mildly hawkish commentary from Fed officials added to the uncertainty, as concerns mounted that the central bank may be headed for a policy mistake in continuing to lower rates. In the absence of official government data, several large investment firms have attempted to fill the gap with employment growth estimates, but with widely divergent results. Data from Carlyle suggested job growth of just 17,000 last month, while a report from Goldman Sachs indicated gains closer to 80,000. In either case, the decline of foreign-born workers risks masking the recent trend of lower payroll growth as only a demand-side issue and could lead to higher wages and inflation if employers struggle to find available workers. Turning to the week ahead, no additional votes on reopening the government are anticipated until at least Tuesday, which means expected economic reports may be further delayed. The U.S. Labor Department announced that it will bring staff back to work on September’s CPI report, which is tentatively scheduled for Wednesday. Retail sales and housing data are not likely to be released without a funding bill. If the shutdown continues, questions could be raised about the Fed’s next rate decision given the lack of access to official economic data. If the shutdown ends, it could be challenging for government agencies to release all the missed data in a timely manner. Meanwhile, earnings season gets underway this week with most of the large U.S. banks reporting along with global technology companies Taiwan Semiconductor and ASML Holdings. On the international calendar, China is scheduled to release trade and inflation figures this week, while the UK has GDP and employment reports. Investors will continue to monitor the political turmoil in France and Japan that is contributing to rising volatility.

CHART OF THE WEEK

Short-term dollar strength

The U.S. Dollar index ($DXY) pressed higher last week, nearing the $100 level for the first time in two months as political upheaval abroad boosted the index. $DXY tracks the dollar against a basket of global currencies, not its purchasing power relative to inflation. Over 70% of the basket is comprised of the euro (57.6%) and the Japanese yen (13.6%), which both weakened last week. The yen sank 3.7% versus the dollar after Japan’s governing party elected Sanae Takaichi as its new leader. Although her ascent to prime minister is not assured, the result signals a potential move towards aggressive fiscal stimulus and a more dovish central bank. Meanwhile, French President Macron was expected to name his sixth prime minister in less than two years late last week, creating more uncertainty and eroding confidence in the EU’s second-largest economy. The euro slid 1.5% against the dollar. From a technical standpoint, $DXY has been trending lower all year, but a bullish MACD divergence did appear at both the July and September lows. The index is now above a rising 50-day exponential moving average for the first time since February. The technical signals are showing signs of a potential near-term bullish reversal, but the trends of U.S. fiscal and monetary policy may still weigh on the greenback over the long term.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.