Weekly Newsletter September 15th to September 19th

RECAPPING LAST WEEK

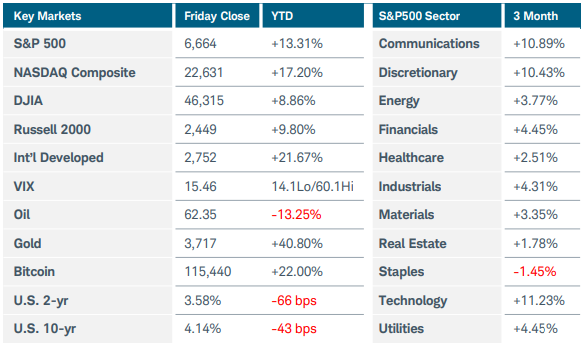

U.S. equity indices gained ground after the Federal Reserve restarted the interest rate easing cycle, lowering its benchmark rate by 25 basis points to a 4.00% to 4.25% range. The Russell 2000 index jumped more than 2%, reaching a new record high for the first time since last November. The Nasdaq Composite index also rose more than 2% while the S&P500 added just over 1%. Technology led mixed performance in S&P500 sectors, boosted by news of Nvidia’s massive investment in Intel. U.S. Treasury yields ended the week flat at the short end and higher at the long end despite the Fed signaling two additional rate cuts for this year. While Fed Chair Powell said that the softening labor market was now top of mind for the committee, the central bank’s statement acknowledged that inflation hasn’t just remained elevated but has moved up. Powell characterized the rate decision as a “risk-management cut” in reaction to weakening jobs data, but stubborn inflation underscores the Fed’s challenges in carrying out its dual mandate. In its Summary of Economic Projections, the FOMC raised its GDP growth and inflation forecasts while lowering the projected unemployment rate, seemingly in conflict with easing monetary policy. The updated “dot plots” suggested only one more rate cut in 2026 to a range of 3.25% to 3.50%, which is higher than market expectations of a sub-3% fed funds rate. Turning to economic data, U.S. retail sales rose 0.6% in August, rounding out a resilient summer of consumer spending. Jobless claims fell back to 231,000, likely confirming that the prior week’s large jump was an anomaly. Regional manufacturing surveys from the northeast revealed widely diverging sentiment. Activity in New York State declined more than expected on a large drop in new orders, while the Philly Fed survey spiked into positive territory as shipments surged. In housing news, new construction plunged last month while building permits fell to the lowest level in more than five years. Mortgage rates fell last week to 11-month lows, but persistent U.S. budgetary and inflation pressures still clouded the outlook for homebuyers seeking more affordable conditions. Overseas, the Bank of England kept rates unchanged at 4% after last month’s CPI reading held steady at 3.8%--the highest among developed economies. UK labor market data has held up well enough to not raise recession concerns. The BOE also announced plans to slow the pace of reducing its stockpile of government bonds to minimize the impact on the volatile gilt markets. The Bank of Canada cut rates by 25 basis points to 2.5% but gave little indication of next steps even as economic data showed signs of increasing stress. Japan’s central bank revealed a more hawkish turn despite leaving rates unchanged at 0.5%. Two of the nine board members voted for a quarter-point hike while the Bank of Japan also decided to start selling its riskier ETF holdings sooner than expected. Core CPI readings have eased recently but Japan’s headline inflation has remained well above the 2% target for more than three years. Finally, China’s industrial production and retail sales figures for August came in lower than estimates, while unemployment inched up to a six-month high of 5.3%.

THE WEEK AHEAD

The U.S. dollar rallied late last week and volatility was mostly subdued, boosted by the Fed’s optimistic economic outlook and a muddled interest rate forecast beyond this year. Whether or not those trends continue could be influenced by several events on this week’s calendar. First, there are a plethora of appearances by FOMC members to be scrutinized. Secondly, Friday’s PCE price index release is expected to show that inflation pressures are continuing to rise, albeit modestly. And third, flash PMI readings in the U.S. and elsewhere will provide a sense of how the manufacturing and services sectors are holding up as the end of the third quarter approaches. Other releases on the U.S. calendar include new and existing home sales, the final estimate of Q2 GDP, durable goods orders, and the goods trade balance for last month. Micron Technology reports earnings on Tuesday followed by Costco on Thursday. On the international side, Japan’s inflation updates and minutes from last week’s BOJ meeting are the notable releases along with the previously mentioned flash PMI readings. Investors will continue to monitor U.S.-China trade negotiations and progress on the government funding bill that passed the U.S. House on Friday but faces an uphill battle in the Senate with the September 30 deadline looming.

CHART OF THE WEEK

Crunch time for chips

The PHLX Semiconductor index (SOX) broke out of its two-month sideways consolidation on September 10 after Oracle rocketed higher by more than 35% higher following impressive forward-looking guidance. Both the index price and the MACD indicator breached above significant technical resistance. Last week’s news of the collaboration between Nvidia and Intel sent the index to its second breakout in as many weeks. A $5 billion investment from the world’s leading chip company along with a co-development partnership resulted in a 23% one-day gain for Intel and a healthy 3.5% rise in Nvidia shares. These two companies make up 17% of SOX on a market-capitalization basis and provided a substantial lift to other components of the index. The SOX ended up rallying 4% on Thursday, reaching the implied target from the consolidation rectangle built over the last two months. Rectangles are typically continuation price patterns, which is how this scenario resolved as SOX had previously been in a strong uptrend coming out of the April lows. Barring a drop back into that consolidation zone, the near-term buying pressure seems likely to continue as typically the fourth quarter is seasonally strong for the group.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.