Weekly Newsletter September 22nd to September 26th

RECAPPING LAST WEEK

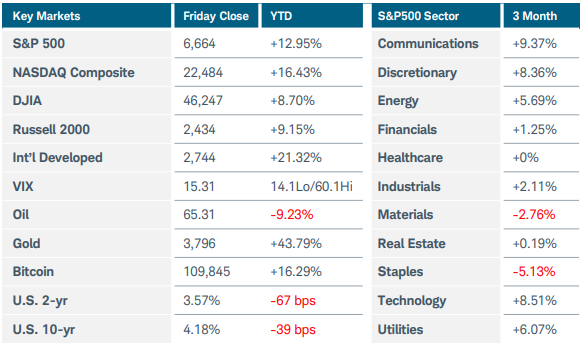

All U.S. equity indices hit record highs last Monday, with momentum fueled by NVDA’s $100B data center investment with OpenAI. Gains faded after Fed Chair Powell flagged stock valuations and second quarter GDP was revised up to 3.8%, tempering expectations for two more rate cuts this year. Major indices ended the week modestly lower, falling less than 1% each. Metals advanced further, with gold rising 2% and silver rocketing higher by more than 7%. Only the energy and utilities sectors managed to stay positive, rising 4% and 2% respectively. The energy rally was supported by surging oil prices amid reduced Russian exports and multiple Ukrainian drone attacks on Russia’s energy infrastructure. U.S. economic data was mixed. Business activity slowed for a second straight month, with S&P Global’s flash composite PMI easing to 53.6 in September, dragged by weaker manufacturing and services. Firms flagged tariffs as the main driver of higher input prices, but weak demand limited their ability to pass through costs. New home sales surged 20.5% in August, the best result in 3 years, but existing home sales were flat. Median home prices increase 2% YoY which appears to be largely a result of investors’ influence--28% of sales were all-cash. Durable goods orders rose 2.9% in August and the goods trade deficit narrowed sharply to $85.5B. Jobless claims came in below expectations at 218k, but continuing claims remained elevated, signaling longer unemployment spells. Inflation held steady with Fridays Core PCE at 2.9%, but expectations are for that to turn higher, with 1-year expectations up to 4.7% helping pull consumer sentiment down to 55.1 from 55.4. Globally, Germany’s flash PMI improved to 52.4, the best result in 16 months, while its business climate index softened to 87.7. The U.K. PMI dipped to 51 amid higher labor and energy costs. In Asia, China held rates steady, Japan’s CPI was flat at 2.5% YoY, and Australia’s CPI rose to 3.0%, leading to doubts that the country would see easing in the near term.

THE WEEK AHEAD

Markets enter October with the focus squarely on the labor market. JOLTS on Tuesday, ADP on Wednesday, nonfarm payrolls, unemployment, and wage data on Friday will set the tone for Fed policy expectations. Inflation remains a central theme. This week’s ISM Manufacturing and Services PMIs will be closely watched for price pressures, while global PMIs from Europe and China are expected to highlight diverging growth trends. Consumer sentiment and wage data may offer clues to how much higher costs are affecting demand. Commodity markets could see added volatility after Wednesday’s OPEC meeting, where any signal on supply cuts would feed into inflation expectations. Other factors to watch include U.S. Treasury auctions across the curve and the upcoming Q3 earnings season, beginning with major banks. Fed commentary and geopolitical developments remain potential swing factors. Together, these events may drive sharp moves across equities, interest rates, and commodities as investors reposition around data and policy risk.

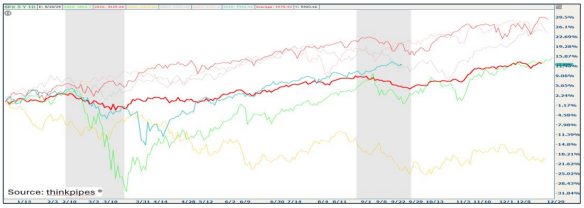

CHART OF THE WEEK

Seasonal anticipation

Seasonal moves in the stock market can often be linked to recurring underlying factors. One way to view these tendencies is through a seasonal chart of the S&P 500 (SPX). By comparing the index’s performance over the past five years (2021-2024), we can see how recent movements align with historical trends. Each year is shown individually: the darker-shaded red line illustrates the average from these years, while the turquoise line shows 2025 SPX performance year-to-date (YTD). Historically, SPX has tended to show seasonal weakness in February/March then again in September. However, this September has so far defied the historical trend. It’s important to note that seasonality reflects long-term averages, not precise forecasts. While seasonality is a historical average of how the S&P 500 tends to perform throughout the year, a study of this nature shouldn’t be interpreted as providing an accurate forecast of what will happen this year. But historically, Q4 tends to be quite strong.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.