Weekly Newsletter September 29th to October 3rd

RECAPPING LAST WEEK

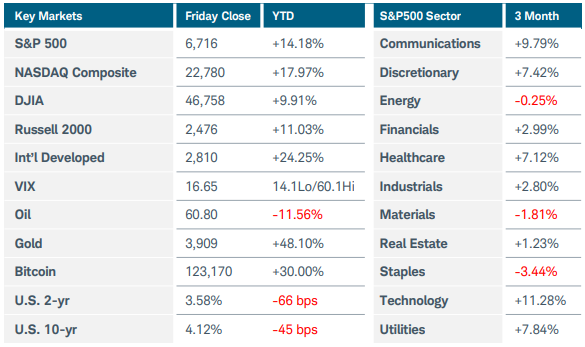

U.S. equity indices recorded yet another weekly record close despite the government shutdown— the fifteenth such stoppage since 1981 and the first since late-2018. The release of the key September jobs report was a casualty of the shutdown, but weakness in other labor market data lifted odds for two additional rate cuts by year-end. The S&P500, Nasdaq Composite, and Russell 2000 indices rose between 1% and 2%. Strong sector performance was dominated by healthcare, which surged nearly 7% after Pfizer reached a deal with the government to lower prescription drug prices in exchange for relief from tariffs that could otherwise have approached 100%. The agreement sparked optimism that other pharmaceutical companies may be able to negotiate favorable outcomes. Sliding oil prices weighed on the energy sector as crude futures tumbled 7% following news that OPEC+ was weighing another production increase at its October 5 meeting. Gold soared 3% to another all-time high above $3,900 while Bitcoin and Ethereum each spiked 12%. U.S. Treasury yields fell after Wednesday’s ADP private payrolls report revealed a reduction of 32,000 jobs last month. The release garnered more attention than usual given the halt in government data reporting and gave investors more confidence that further rate cuts are forthcoming. According to the JOLTS report, job openings increased only marginally in August while hiring declined. This year has seen employers announce more job cuts than in any year since 2020, while hiring plans are the lowest since 2009. A new “real-time” estimate from the Chicago Fed stated that the unemployment rate was likely unchanged at 4.3%. In other economic news, U.S. consumer confidence worsened this month as concerns over job availability mounted. The ISM manufacturing PMI edged up to 49.1 in September, although new orders and employment remained subdued and prices paid were still elevated. ISM services PMI fell to 50.0 from 52.0 the prior month. On the international side, inflation in Germany and the wider Eurozone accelerated last month to +2.4% and +2.2%, respectively. Economic trends suggested this was a temporary uptick and the European Central Bank is predicted to keep rates steady later this month. Australia’s central bank held its benchmark rate at 3.6%, acknowledging that economic and inflation data has firmed. In China, September’s manufacturing PMI was the strongest in six months, driven by gains in output and new orders. Last of all, sentiment among Japan’s large manufacturers improved for a second straight quarter, strengthening the case for the Bank of Japan to raise rates. A hawkish shift emerged at last month’s BOJ meeting, with markets pricing in around a 60% chance of a hike at the October 30 gathering.

THE WEEK AHEAD

Historically, U.S. government shutdowns have not had a significant impact on the economy, and any lost activity is typically recovered fairly quickly. However, the delayed publication of key reports could impact both investors and FOMC policymakers. If the shutdown lasts a few weeks or more, important releases like CPI, PPI, retail sales, and housing data may not be published. With the Fed having emphasized data dependence heading into its next rate decision at month end, investors may need to brace for rising volatility if the interest rate path becomes less clear. Additionally, tariff concerns persist with new levies announced last week on heavy-duty trucks, kitchen and bathroom materials, and home furniture. On this week’s economic calendar, reports that may be impacted by the shutdown include the U.S. trade balance and consumer credit figures along with weekly unemployment claims. Treasury auctions have typically not been postponed by prior shutdowns, and there are 10- and 30-year sales scheduled for Wednesday and Thursday. Minutes from the last FOMC meeting also arrive mid-week while Friday brings the University of Michigan’s preliminary consumer sentiment reading and inflation expectations for September. Third-quarter earnings season won’t begin in earnest until the week of October 13 but reports on Thursday morning from Delta Airlines and Pepsico may provide insight into consumer spending trends. Overseas, most of the economic news will flow from Europe with several low to medium-impact reports. German factory orders and industrial production along with EU retail sales and investor confidence are on the docket. Minutes from the last ECB and Bank of England meetings round out the calendar. The Japanese yen rallied last week amid rate hike speculation, but the outcome of the ruling party’s leadership election over this past weekend is crucial as the two candidates have opposing views on fiscal and monetary policy.

CHART OF THE WEEK

Precious indeed

Gold and silver have jumped 48% and 64%, respectively, year to date. The convergence of macro, geopolitical, and structural demand factors have been strong tailwinds but there are distinct characteristics pushing each one forward. One that they have in common is de-dollarization. The dollar has underperformed this year despite high nominal interest rates and that trend looks likely to continue, pushing capital to other asset classes like precious metals. The largest buyers, especially for gold, have been central banks. China, India, Russia, and others are starting to move away from traditional safe-haven assets like U.S. Treasuries, and they tend to be regular buyers of gold without much price sensitivity. Silver is supported by industrial demand, specifically in solar panels, batteries, and data centers. It should be no surprise that the mining companies are at record highs as well. The PHLX Gold and Silver Index (XAU), which tracks the top miners in the space, is up 115% in 2025. The uptrend accelerated mid-year and has maintained its steeper incline. The MACD indicator continues to rise while the RSI has been in overbought territory for over a month. That leads to the possibility of short-term pullbacks but so far investors have aggressively bought those opportunities.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.