Weekly Newsletter September 8th to September 12th

RECAPPING LAST WEEK

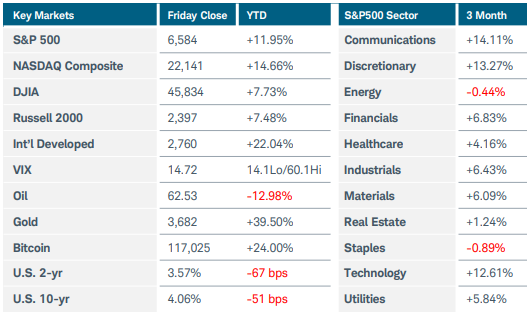

U.S. equity indices continued their ascent into record territory amid inflation and employment data that all but confirmed that the Federal Reserve is set to resume cutting interest rates. The Nasdaq Composite index gained 2% while the S&P500 rose 1.6%, and Russell 2000 added 0.3%. Ten of eleven S&P500 sectors finished positive, led by a 3% jump in technology. Gold maintained its parabolic rise, trading above $3,700 before settling near $3,685. Oil was up 1% for the week despite a bearish report from the International Energy Agency, which suggested the potential for massive oversupply in the year ahead. The possibility of production interruptions in the near term after Israel’s attack on Hamas leadership in Qatar and talk of additional sanctions on Russian exports were supportive for oil prices. U.S. Treasury yields fell after more evidence emerged that the labor market has been softening for some time. The government’s annual benchmark revision to nonfarm payrolls data suggested that the U.S. economy created 911,000 fewer jobs than previously estimated in the twelve months through March 2025. Worker confidence in the ability to move jobs fell to 44.9%, the lowest reading in the history of the New York Fed’s Survey of Consumer Expectations that dates to 2013. There was also a spike in jobless claims for the first week of September, although it may have been a temporary blip due to an outsized increase in Texas. On the inflation front, U.S. CPI rose 0.4% MoM and 2.9% YoY in August, above estimates but likely not high enough to derail the much-anticipated upcoming rate cut. Producer prices fell 0.1%, reversing a surprise jump from the prior month. September’s preliminary consumer sentiment reading declined to 55.4 from 58.2, the lowest level since May. One-year inflation expectations were unchanged at 4.8% while the long-term rate rose to 3.9% from 3.5%. U.S. consumers expressed concerns for the jobs market and high prices for goods and services. Overseas, the European Central Bank held its benchmark rate at 2%, offering no hints about its next move despite lowering inflation forecasts. ECB President Lagarde may have to manage expectations carefully given France’s fiscal troubles that have spooked bond investors. In the UK, GDP growth stalled to begin the year’s second half as headwinds from rising inflation persisted. Japan’s long-term bond yields reached record highs after prime minister Ishiba’s resignation raised fears that potential successors may shift to more dovish fiscal policies—further stressing the world’s most indebted advanced economy. Finally, China’s export growth slowed to 4.4% YoY in August, but the country remained on track for a record trade surplus this year. Exports to other Asian nations have more than compensated for five straight months of double-digit declines in U.S. shipments. China’s deflation in producer prices slowed last month after the government started to rein in excessive competition and price cuts in key industrial sectors.

THE WEEK AHEAD

Central banks will dominate the headlines this week, with interest rate decisions due in the U.S., Canada, Britain, and Japan. There are slim hopes for a 50-basis point cut from the FOMC on Wednesday, but a more modest quarter-point reduction seems to be the likely outcome. Chair Powell’s press conference and the updated “dot plot” and Summary of Economic Projections will be the focus for investors. Fed funds futures are essentially pricing in two additional cuts by year end, so the question will be if the FOMC’s projections match the market’s dovish expectations. If not, volatility may make an appearance. The U.S. economic calendar this week features retail sales, manufacturing surveys from the northeast regions, and housing starts and building permits. The Bank of Canada meets Wednesday, with a quarter-point rate reduction expected and another priced in for later this year. The Bank of England, after lowering rates last month in a close decision, faces a much tougher task this week given the recent rise in inflation. August’s CPI release on Wednesday will precede the BoE meeting. In Japan, odds for a rate hike at Thursday’s meeting have fallen below 50% after Ishiba’s resignation. However, investors are still optimistic for action by year end after the central bank said economic conditions are developing as expected. China’s monthly industrial production and retail sales figures round out the international agenda.

CHART OF THE WEEK

Rate reversal

Recently, U.S. Treasury yields have fallen sharply as a softening labor market has made short-term interest rate cuts more likely while also heightening concerns for a slowing economy. Looking at yields from a technical perspective, the Cboe 10-year Treasury Note Yield index (TNX:CGI)—which measures the 10-year yield multiplied by 10—broke below an important support level near $42 after the September 5 jobs report. The index briefly fell below $40 (4.0% yield) last week for the first time since the early April lows. With the Federal Reserve set to cut rates for the first time in nine months at the September 17 meeting, TNX could remain under pressure. For the time being, employment is taking precedence over inflation as the Fed considers its dual mandate. Last week’s inflation data was mixed—producer prices fell in August after jumping the prior month, while consumer prices remained elevated but in-line with expectations. Inflation isn’t spiking as much as many forecasted it would from tariffs, but it is still well above the Fed’s 2% target and not coming down. This could continue to weigh on consumer sentiment and keep inflation expectations high, which in turn could put upward pressure on longer-term yields. The prior technical support near $42 on TNX may act as resistance if yields start to rally again at some point. Falling rates have been a tailwind to other assets like gold and equities, which are both at all-time highs, but this week’s FOMC meeting could impact whether these trends continue.

Source: Charles Schwab Corporation

IMPORTANT LEGAL NOTICE AND DISCLOSURE INFORMATION

Investment advisory service is provided by SVL Holding Corporation dba SVL Investments Management (“SVL”), a California registered investment advisor. Advisory services are subject to advisory fees as disclosed on Form ADV.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended or undertaken by SVL) or product made reference to directly or indirectly by SVL in its web site, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by SVL), or any non-investment related content, made reference to directly or indirectly on this site will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results for investment indices.

Certain portions of SVL‘s web site (i.e. blog, Insights, newsletters, articles, commentaries, etc.) may contain a discussion of, and/or provide access to, SVL‘s (and those of other investment and non-investment professionals) positions and/or recommendations as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from SVL or from any other investment professional. SVL is neither an attorney nor accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.

Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if SVL is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of SVL by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser.

To the extent that any client or prospective client utilizes any economic calculator or similar device contained within or linked to SVL‘s web site, the client and/or prospective client acknowledges and understands that the information resulting from the use of any such calculator/device, is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from SVL, or from any other investment professional.

Each client and prospective client agrees, as a condition precedent to his/her/its access to SVL‘s web site, to release and hold harmless SVL, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from SVL.